Introduction

Payroll runs late. A vendor payment reverses without warning. A recurring billing batch fails and no one knows why. In most cases, the culprit is the same: a gap in how the ACH network actually works.

ACH handles the bulk of scheduled, bank-to-bank transactions in the U.S. — payroll, vendor disbursements, recurring billing, tax payments.

The scale is hard to overstate. According to Nacha's 2025 statistics, the ACH Network processed 35.19 billion payments valued at $93 trillion last year, a 7.9% increase in value from 2024. B2B transactions drove much of that growth: 8.08 billion B2B ACH payments totaling $63.11 trillion, up 9.9% in volume year-over-year.

Despite this volume, most finance and operations teams only interact with ACH at the surface level: initiating a payment or receiving a deposit without understanding what happens in between.

That gap has real consequences. Missed cut-off times delay payroll, unexpected returns reverse settled funds, and teams make poor calls about when ACH is the right method.

This guide breaks down how ACH processing works — from initiation through settlement — so your team can avoid the errors that cost time and money.

Key Takeaways

- ACH is a batch-based, bank-to-bank payment network governed by Nacha — used for payroll, vendor payments, and recurring billing

- Payments move through four stages — from originator initiation to final RDFI settlement

- Standard ACH settles in one to two business days; Same Day ACH settles within hours but has strict cut-off requirements

- ACH credits are "push" payments (sender-initiated); ACH debits are "pull" payments (receiver-initiated)

- ACH is typically the lowest-cost electronic payment method — significantly cheaper than wires or card transactions

What Is ACH Payment Processing?

ACH payment processing is the electronic transfer of funds between U.S. bank accounts using the Automated Clearing House network — a centralized infrastructure governed by Nacha that connects every U.S. bank and credit union. It was built to replace paper checks with a faster, more reliable alternative for recurring and scheduled payments.

What ACH Is Not

ACH is often confused with faster or more complex payment methods. Here's how it differs:

- Wire transfers (Fedwire) settle individually in real time, one transaction at a time — ACH batches multiple payments together and processes them on a schedule

- Card payments use separate card networks (Visa, Mastercard) with their own authorization and clearing infrastructure

- Instant payment rails like FedNow and The Clearing House's RTP settle in seconds, 24/7 — ACH operates on banking-day windows only

ACH trades raw speed for volume capacity and low transaction costs, making it well-suited for recurring and scheduled payments rather than time-sensitive transfers.

ACH Credits vs. ACH Debits

Every ACH transaction is one of two types:

| Type | Direction | Who Initiates | Common Example |

|---|---|---|---|

| ACH Credit | Push | Sender | Payroll direct deposit |

| ACH Debit | Pull | Receiver | Subscription billing, utility auto-pay |

Both follow the same network path. The difference is who plays the role of originator — and for debits, the account holder must provide prior written or electronic authorization before any funds can be pulled.

How Does ACH Payment Processing Work?

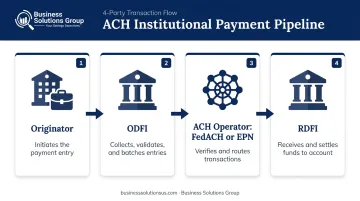

ACH operates as a sequential, batch-based process involving multiple institutional parties — here's how each stage unfolds.

Initiation

The process starts when the originator, a business, employer, or government agency, authorizes a payment entry with these required details:

- Account holder name

- Bank routing number

- Account number

- Transaction amount

- Payment type (credit or debit)

Initiation can be a one-time manual entry (a vendor payment) or fully automated (recurring payroll). For debit transactions specifically, the originator must have the account holder's prior authorization — a signed or electronically confirmed mandate — before pulling funds.

ODFI Collection and ACH Operator Routing

Once initiated, the payment enters the institutional pipeline:

- The Originating Depository Financial Institution (ODFI) collects payment entries from the originator, validates them, and bundles them into batch files

- The ODFI submits these batch files to one of two ACH operators — the Federal Reserve Banks (FedACH) or The Clearing House's Electronic Payments Network (EPN)

- The ACH operator verifies the batch and routes individual payment entries to each Receiving Depository Financial Institution (RDFI)

Because every U.S. bank and credit union participates, the network is universally interoperable — an ACH payment can reach any domestic bank account.

Cut-off times matter here. Each ODFI has submission deadlines throughout the day. The FedACH service runs 11 daily processing windows — three same-day windows and six future-day windows, plus two intraday return windows. Miss your ODFI's cut-off and the batch rolls to the next window or the following business day.

Settlement and Returns

The RDFI receives routed payment entries and credits or debits customer accounts accordingly. The Federal Reserve's National Settlement Service settles funds four times daily, as Nacha's ACH overview confirms.

If the RDFI identifies a problem — insufficient funds, a closed account, or an incorrect account number — it sends an ACH return code back to the ODFI, which reverses the transaction. Return windows by entry type:

- Corporate (B2B) entries: Standard return window is two banking days

- Consumer entries: Unauthorized transactions can be returned up to 60 calendar days after settlement

That 60-day consumer return window is why businesses shouldn't release goods or services solely based on an ACH debit clearing — the payment can still come back.

How Long Does ACH Processing Take?

ACH timing isn't fixed — it depends on when you initiate, your ODFI's cut-off schedule, and which settlement window your batch hits.

Standard ACH

Most ACH payments settle within one to two business days. Nacha's network supports same-day, next-day, and up-to-two-business-day scheduling. Payments submitted after the last daily cut-off won't enter processing until the next business day.

Same Day ACH

Launched in September 2016 for credits (debits followed in 2017), Same Day ACH allows payments to settle on the same banking day when submitted before the applicable cut-off. Key details for the three FedACH same-day windows (1:00 p.m., 5:00 p.m., and 6:00 p.m. ET):

- Per-payment limit: $1 million — sufficient for most B2B transactions

- Approved increase: Nacha has approved a $10 million limit, effective September 17, 2027

- Fee: Same Day ACH carries a higher per-item fee than standard ACH

Weekends and Federal Holidays

ACH settlement only occurs on banking days when the Federal Reserve's settlement service is open. Payments due on a weekend or federal holiday follow different rules:

- Payroll: If a payday falls on a non-banking day, funds are typically settled the prior Friday

- Bill payments/debits: Collections due on a non-banking day are processed on the next banking day

Factor this into your payroll and vendor payment schedules. A Friday submission intended for Monday delivery will arrive Tuesday if Monday is a federal holiday.

Where Businesses Use ACH Payments

ACH works best for scheduled, recurring, or high-value payments between known counterparties. The primary use cases:

- Payroll direct deposit — the most common ACH application for employers

- Recurring vendor and supplier payments — predictable disbursement cycles

- Accounts payable — bulk payment runs to multiple suppliers

- Subscription and SaaS billing — pulling recurring fees from customer accounts

- Government transfers — tax payments, benefit disbursements, grant funding

ACH is not suited for point-of-sale transactions where authorization needs to happen in seconds. It also isn't designed for one-time payments to unknown counterparties where return risk is high.

ACH use is expanding into newer contexts as well: ecommerce checkout (account-to-account payments), BNPL installment collection, account funding transfers, and real-time balance verification flows. These applications trade on ACH's low cost while accepting its timing constraints.

ACH performs best for businesses with predictable payment cycles, established banking relationships, and back-office systems (ERP, accounting software) that integrate with ACH data. Because ACH transaction data is highly structured, reconciliation and bookkeeping are cleaner and easier to automate than with paper checks.

Benefits of ACH Payments for Businesses

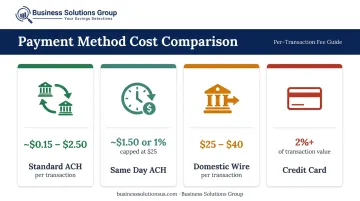

Cost Advantage

ACH is the lowest-cost electronic payment method available for most business transactions. A direct comparison using published bank fee schedules illustrates the gap:

| Payment Method | Representative Fee Range |

|---|---|

| Standard ACH | ~$0.15–$2.50 per transaction (Chase business rates) |

| Same Day ACH | ~$1.50 per item (Wells Fargo) or 1% capped at $25 (Chase) |

| Domestic wire (outgoing) | $25–$40 per transaction (Chase/Wells Fargo) |

| Credit card processing | ~2%+ of transaction value |

For a business running 500 vendor payments a month, switching from wires to standard ACH can reduce per-payment costs by 90% or more. At scale, that adds up to tens of thousands of dollars annually.

Security and Compliance

Nacha rules require encryption for ACH data transmitted over public networks, and covered originators must render stored account data unreadable — through encryption, tokenization, truncation, or destruction. ACH debit transactions also require pre-authorization from the account holder, creating a documented approval trail before any funds move.

Compare that to paper checks: the AFP's 2026 Payments Fraud and Control Survey found that 58% of organizations reported check fraud in 2025, with checks remaining the payment method most frequently targeted by fraud — well ahead of ACH.

Advisory Support for Payment Optimization

Getting the payment mix right is rarely a standalone decision. Business Solutions Group works with clients to identify where payment and supply chain process inefficiencies are driving unnecessary costs — and ACH adoption is often one piece of a larger initiative, alongside vendor contract renegotiation, invoice automation, and payment method optimization.

A complimentary savings analysis can pinpoint exactly where current payment workflows are costing more than they should.

Conclusion

ACH payment processing follows a clear sequence: a business initiates a payment entry, the ODFI bundles and submits it to an ACH operator, the operator routes it to the receiving bank, and the RDFI settles funds during one of four daily windows. The concept is straightforward, but timing, cut-off schedules, and return risk mean the details matter more than they appear.

That understanding directly affects outcomes: businesses that know the mechanics can schedule payments accurately, avoid costly errors, and match the right method to each transaction type. For high-volume recurring payments, ACH's combination of low cost, structured data, and broad reach makes it the practical default — one that becomes more valuable as B2B payment volumes grow and same-day settlement windows expand.

Frequently Asked Questions

How long do ACH payments usually take to process?

Standard ACH settles within one to two business days, depending on your ODFI's cut-off schedule. Same Day ACH can settle within hours — provided you initiate before one of the three FedACH same-day windows (1:00 p.m., 5:00 p.m., or 6:00 p.m. ET).

Do all U.S. banks support ACH payment processing?

Yes — every U.S. bank and credit union participates in the ACH network, making it universally reachable. Businesses typically access ACH processing through their bank directly or through a third-party payment processor that interfaces with their ODFI.

What information is needed to initiate an ACH payment?

You need the account holder's name, bank routing number, account number, transaction amount, and payment type (credit or debit). For ACH debit transactions, you must also have prior written or electronic authorization from the account holder before pulling funds.

What is the difference between ACH credit and ACH debit?

ACH credits are push payments — the sender initiates the transfer, as with payroll direct deposit. ACH debits are pull payments — the receiver initiates the withdrawal from the customer's account, as with recurring subscription billing or utility auto-pay.

Can an ACH payment be reversed or cancelled?

Scheduled payments can be cancelled before they enter processing. Once settled, reversals are permitted only for specific errors — duplicate payments, wrong account, incorrect amount — and must be initiated within five banking days of the settlement date. That window closes fast, so flag errors as soon as they appear.

How do ACH fees compare to credit cards and wire transfers?

ACH is consistently the lowest-cost option. Standard ACH runs roughly $0.15–$2.50 per transaction at major banks, while outgoing domestic wires typically cost $25–$40 per transaction and credit card processing runs 2% or more of the transaction value. For high-volume recurring payments, the difference compounds quickly.