The math is straightforward and uncomfortable: at a 2–3% effective rate, a business processing $5 million in annual card volume pays $100,000–$150,000 in fees. At $10 million, that's $200,000–$300,000. For most companies, that's not a rounding error — it's a material margin drain hiding in plain sight on monthly processing statements.

What makes this particularly frustrating is that these costs aren't fixed. They're shaped by pricing model choices, operational habits, transaction data quality, and whether you've ever looked closely enough at your statements to know what you're actually paying. Most businesses haven't.

This article covers where B2B processing fees originate, what drives them higher than necessary, and three categories of strategies to reduce them — without abandoning card acceptance or straining buyer relationships.

Key Takeaways

- B2B credit card fees (typically 1.5%–3.5% per transaction) run higher than B2C due to corporate card types, large ticket sizes, and Level 2/3 data requirements

- Fees stack across interchange, assessments, and processor markup — and most businesses overpay due to poor data practices or opaque pricing models

- The highest-leverage fixes are structural: switching pricing models, submitting Level 2/3 data, and routing high-value invoices to ACH

- Operational habits like batch timing, AVS checks, and card-present entry silently inflate or protect your effective rate

- Surcharging, convenience fees, and ACH incentives can shift the cost burden without touching your processor contract

How B2B Credit Card Processing Fees Build Up

Processing fees aren't a single line item. Every card transaction passes through three distinct cost layers:

| Layer | Who Gets Paid | Negotiable? |

|---|---|---|

| Interchange | Issuing bank | No — set by card networks |

| Assessment | Card network (Visa, Mastercard) | No — fixed rates |

| Processor markup | Your processor or acquirer | Yes |

Interchange is typically the largest component. As Mastercard explains, it's one component of the merchant discount rate — the total rate your acquirer charges — and it varies by card type, transaction method, and data quality.

Why B2B Statements Are Hard to Read

The problem isn't just that fees are high. Tracking them without a deliberate audit is nearly impossible. Monthly statements often contain dozens of line items — interchange categories, batch fees, gateway charges, PCI fees, monthly minimums — presented inconsistently across processors.

Most businesses never calculate their true effective rate. Without that number, there's no way to know whether you're paying a fair price or an inflated one.

Where B2B Costs Diverge From B2C

Three structural factors push B2B processing costs above consumer averages:

- Corporate and purchasing cards carry higher interchange rates than standard consumer cards

- Percentage-based fees on $10,000+ invoices produce large dollar amounts even at modest rates

- Missing Level 2/3 transaction data triggers automatic downgrades to higher-cost interchange tiers, with no alert from your processor

Key Cost Drivers for B2B Credit Card Processing Fees

Four structural factors drive B2B processing costs higher — and knowing which ones you can actually control changes how you approach them.

Card Type Is Largely Out of Your Control

Business rewards cards, corporate cards, and purchasing cards all carry higher interchange than standard consumer cards. Visa's published interchange schedule shows business credit categories ranging from 1.90% to 3.15% + $0.10, depending on product tier — before any processor markup. You can't tell a buyer which card to use, making card mix a structural cost factor rather than an operational one.

Transaction Method and Data Quality Determine Tier Qualification

This is where operational choices have direct rate consequences. From Visa's current interchange schedule:

- Commercial Card Present: 2.50% + $0.10

- Commercial Card Not Present: 2.70% + $0.10

- Commercial Level III (with enhanced data): 1.90% + $0.10

- Commercial Non-Qualified (downgraded): 2.95% + $0.10

That's a 105 basis point spread between a well-processed transaction with Level 3 data and a downgraded one. On a $50,000 monthly card volume, that difference exceeds $600 per month — over $7,500 annually.

Pricing Model Obscures the True Cost

Most small and mid-sized B2B businesses are on tiered or bundled pricing models, which group transactions into "qualified," "mid-qualified," and "non-qualified" buckets. This structure hides where costs actually originate.

Interchange-plus pricing passes through the actual interchange rate with a separate, visible processor margin — making benchmarking and negotiation straightforward.

The Compounding Problem

These factors don't operate in isolation. A business can face every unfavorable condition at once:

- Accepting high-interchange corporate cards

- Processing orders by phone (card-not-present)

- Skipping Level 2/3 data submission

- Operating on a tiered pricing plan

Each condition layers additional cost onto the last. The same transaction volume, processed with better practices, could cost materially less — which is exactly what the rest of this guide addresses.

Cost-Reduction Strategies for B2B Credit Card Processing Fees

Not every strategy applies equally to every business. The right sequence depends on your transaction volume, card mix, how payments are currently processed, and your relationships with buyers. What follows is organized by where the lever operates — structural decisions, daily processing habits, or the broader context of how card acceptance is offered.

Strategies That Reduce Costs by Changing Decisions

These are typically one-time, high-leverage changes with lasting impact.

Switch to interchange-plus pricing. Tiered and bundled pricing obscure what you're actually paying. Interchange-plus passes through the actual interchange rate with a fixed processor margin — giving you full visibility to benchmark, negotiate, and identify where costs originate. According to CardFellow, businesses switching from bundled to pass-through pricing can see average cost reductions around 40%, though results vary by transaction profile.

Audit your statements and eliminate junk fees. Most statements contain charges unrelated to interchange — PCI non-compliance fees, batch fees, gateway fees, inactive account fees, and monthly minimums. Many are negotiable or removable without switching processors, making a statement audit the fastest way to recover cost.

Business Solutions Group offers a no-cost, line-by-line statement review that benchmarks your costs against comparable businesses — identifying hidden markups and excessive charges, typically within 3–5 business days.

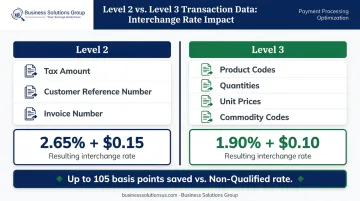

Submit Level 2 and Level 3 transaction data. For corporate and purchasing card payments, submitting enhanced data fields qualifies transactions for materially lower interchange rates:

- Level 2 adds tax amount, customer reference number, and invoice number

- Level 3 adds line-item detail: product codes, quantities, unit prices, commodity codes

The rate difference is significant. Visa's Level III rate of 1.90% + $0.10 is 80 basis points below the standard Card Not Present rate and over 100 basis points below Non-Qualified. Many businesses leave this reduction on the table simply because their payment systems don't capture or transmit these fields automatically.

Shift high-dollar invoices to ACH by policy. According to Nacha, the median cost of initiating and receiving an ACH payment is $0.26–$0.50. Compare that to Visa's commercial card-not-present interchange alone at 2.70% + $0.10 — on a $10,000 invoice, that's $270 in interchange before assessments or markup. ACH fees don't scale with invoice size. Setting a threshold above which card payments either aren't accepted or incur a surcharge shifts the most expensive volume off card rails entirely.

Once structural decisions are locked in, how your team handles transactions day-to-day determines whether those savings hold.

Daily Processing Habits That Protect Your Rate

These operational practices can quietly raise or protect your effective rate — often without anyone noticing until the damage accumulates.

Prioritize card-present entry; avoid manual keying. Interchange is priced around fraud risk, so card-not-present transactions cost more. EMV chip/tap terminals reduce that exposure where in-person acceptance is possible. Where it isn't, digital invoice links with embedded payment options typically carry lower fees than manually keyed entries.

Use AVS/CVV verification and batch daily. Two low-effort habits with compounding impact:

- Failing AVS/CVV checks on phone or online orders can trigger interchange downgrades

- Unsettled transactions after 24 hours downgrade to higher-cost tiers

Neither requires new technology. Both require consistency.

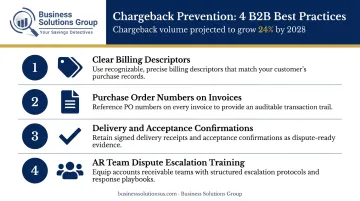

Manage chargebacks proactively. Global chargeback volume is projected to grow 24% from 2025 to 2028, reaching 324 million annual transactions. In B2B, they're less frequent but more damaging — generating penalty fees, consuming AR time, and potentially triggering elevated risk classifications. Prevention costs less than dispute resolution:

- Use clear, recognizable billing descriptors

- Require purchase order numbers on invoices

- Maintain delivery and acceptance confirmations

- Train AR teams to resolve disputes before they escalate

Use payment terms to steer buyers toward lower-cost methods. Early payment discounts — 2/10 Net 30 is the classic structure — reward buyers who pay quickly via ACH or EFT. Making ACH the default and card the exception gradually shifts transaction mix toward lower-cost rails without forcing buyers to change behavior abruptly.

With processing habits optimized, the final lever is how card acceptance is structured and presented to buyers.

Structural Changes to How Card Acceptance Is Offered

These modify how card payments are offered, priced, or positioned — rather than how they're processed.

Implement a credit card surcharge or cash discount program. Surcharging passes the cost of card acceptance to buyers who choose to pay by card. Visa requires 30-day advance notice to your acquirer and caps the surcharge at the lower of your effective acceptance cost or 3%. Cash discount programs work in reverse — advertising a reduced price for non-card payments.

Before implementing either:

- Verify legality in your operating states (Connecticut, Maine, Massachusetts prohibit surcharging; Colorado caps it at 2%)

- Post required signage and disclose on receipts

- Confirm your processor supports the program

Add a convenience fee for non-standard payment channels. Card networks permit a flat convenience fee when a card is used in a channel that isn't your standard method — for example, phone payment when in-person is the default. Unlike surcharges, convenience fees apply to all payment types in that channel, not just cards. This helps offset acceptance costs in specific situations without requiring a full surcharge program.

Offer positive incentives for ACH and EFT payments. Rather than penalizing card use, reward bank-based payments with extended net terms, modest discounts, or streamlined checkout. Over time, this shifts the payment mix toward lower-cost channels without creating friction in buyer relationships.

Conclusion

Most B2B businesses overpay on processing fees not because the savings aren't there, but because no one has mapped exactly where the costs originate. Understanding your fee structure, auditing what's actually being charged, and making a few targeted structural decisions can reduce costs for years.

Fee reduction is also an ongoing discipline. Rates change, card mixes shift, and processors add new charges between billing cycles. Businesses that audit statements regularly, benchmark against industry norms, and fold payment strategy into broader cost goals consistently outperform those that treat processing fees as fixed overhead.

The core actions that move the needle most:

- Negotiate interchange-plus pricing to replace opaque bundled rates

- Qualify transactions at Level 2 or Level 3 to reduce interchange costs

- Audit monthly statements for new fees, surcharges, and misclassified transactions

BSG's no-cost Detailed Savings Analysis Report is a practical starting point — a line-by-line review of your current processing costs benchmarked against what comparable businesses actually pay, with no obligation to act on the findings.

Frequently Asked Questions

Is it illegal to charge a 3% credit card fee to customers?

Credit card surcharges are legal in most U.S. states but regulated. Visa caps surcharges at the lower of your acceptance cost or 3%, and states including Connecticut, Maine, Massachusetts, and Colorado restrict or prohibit them entirely. Businesses must provide 30-day advance notice to their processor and post proper signage before implementing any surcharge program.

How can B2B companies reduce payment friction?

Reducing friction means offering multiple payment options (ACH, virtual cards, credit), providing digital invoices with embedded payment links, and setting clear payment terms with automated reminders. These practices improve on-time payment rates and reduce administrative burden on both AR teams and buyers.

What is the difference between Level 2 and Level 3 data, and how do they lower interchange fees?

Level 2 data adds fields like tax amount and customer reference number; Level 3 goes further with line-item detail such as product codes, quantities, and unit costs. Submitting these fields on eligible corporate card transactions signals lower risk to card networks, qualifying transactions for interchange rates up to 105 basis points lower than non-qualified rates on Visa.

What is interchange-plus pricing, and why does it matter for B2B businesses?

Interchange-plus passes through the actual interchange rate charged by the card network plus a fixed processor margin, making the full cost structure transparent and auditable. Tiered or bundled pricing hides true costs inside qualified/mid-qualified/non-qualified buckets. Interchange-plus eliminates that ambiguity, letting businesses see exactly what they're paying and benchmark it against industry norms.

Are ACH payments always cheaper than credit cards for B2B transactions?

ACH fees typically run $0.26–$0.50 per transaction regardless of invoice size, making them far more cost-effective for large B2B payments. However, standard ACH settles in 1–3 business days and requires bank account information, so most businesses use it selectively for high-value, recurring, or non-urgent payments rather than as a universal replacement for cards.

How often should B2B businesses audit their credit card processing statements?

At minimum, a quarterly review of processing statements helps identify junk fees, track effective rate trends, and catch interchange downgrades early. Annual competitive benchmarking against alternative processors is also advisable — particularly as transaction volume grows or your payment mix changes significantly.