A vendor survey of 350 small businesses found that 37% believe they overpay for credit card processing fees — and nearly half don't even know their actual rate. Meanwhile, U.S. merchants paid a combined $187.20 billion to accept card payments in 2024, according to the Nilson Report. Even a small percentage of unnecessary charges within that figure represents enormous losses at the business level.

This article breaks down how the fee structure actually works, which hidden charges are most common, how to spot overcharging on your statements, and what concrete steps you can take to reduce what you're paying.

Key Takeaways

- Credit card processing fees have three layers: interchange, assessment, and processor markup — yet most merchants only see a single blended total on their statement

- Tiered pricing models create the most opportunity for hidden charges and inflated costs

- Your effective rate (total fees ÷ card volume × 100) reveals whether you're overpaying

- Chargeback fees run $20–$100 per dispute regardless of outcome; early termination fees often reach $295–$495

- Switching to interchange-plus pricing and auditing 6–12 months of statements often reveals immediate, actionable savings

How Merchant Credit Card Processing Fees Actually Work

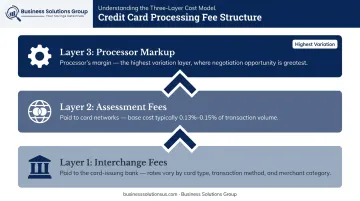

The Three-Layer Fee Structure

Every card transaction involves three separate cost layers, though most statements show only a single blended number:

- Interchange fees — Paid to the card-issuing bank. Rates vary by card type, transaction method, and business category; Visa and Mastercard publish them publicly.

- Assessment fees — Paid to the card networks (Visa, Mastercard). The U.S. Chamber of Commerce notes these have base costs around 0.13%–0.15%

- Processor markup — The payment processor's own margin, layered on top of the other two. This is where the most variation — and the most opportunity for overcharging — exists

Merchants don't pay interchange directly. They pay a negotiated merchant discount rate to their processor, which bundles all three layers. That bundling obscures each component's cost — and sets the stage for the pricing model your processor uses to determine what you actually owe.

Pricing Models: Where Transparency Varies

| Model | How It Works | Transparency Level |

|---|---|---|

| Flat-rate | One fixed rate for all transactions | High — simple, predictable |

| Interchange-plus | Actual interchange cost + fixed processor markup | High — each component is visible |

| Tiered | Transactions sorted into qualified/mid-qualified/non-qualified buckets | Low — markups are obscured |

Tiered pricing is the most common source of unexpected costs. The processor decides which "tier" each transaction falls into — and anything outside the narrow "qualified" criteria gets pushed into higher-cost tiers without your knowledge.

According to the Washington State Attorney General, switching from tiered to interchange-plus pricing can save merchants up to 25% monthly. Understanding which model your processor uses is the first step toward spotting where those savings are being left on the table.

The Most Common Hidden Fees in Merchant Credit Card Processing

Non-Qualified Surcharges

Under tiered pricing, transactions that don't meet "qualified" criteria get reclassified into higher-cost tiers. Common triggers include:

- Rewards cards and travel cards

- Corporate or purchasing cards

- Manually keyed card-not-present entries

- Transactions missing required data fields

Visa's published interchange schedule lists a "Non-Qualified Consumer Credit" rate of 3.15% + $0.10 — compared to far lower rates for standard qualified transactions. For merchants with a high mix of rewards cardholders, this difference adds up fast.

Monthly and Annual Account Fees

These appear under labels like "service fee," "account maintenance fee," or "statement fee." Typical ranges:

- Monthly service fees: $15–$30/month (Business.com)

- Subscription-based processor models: $49–$199/month (Bankrate)

Because they're fixed line items billed separately from transaction costs, they rarely trigger a second look — even as they quietly drain $180–$360 or more per year.

PCI Compliance and Non-Compliance Fees

PCI DSS compliance requires an annual self-assessment questionnaire. Processors charge a fee for the compliance program itself. The more expensive problem: if you haven't completed your assessment, many processors charge a monthly non-compliance penalty — often without notifying merchants it's being applied.

Beyond the fee itself, the PCI Security Standards Council warns that merchants who suffer breaches risk financial penalties, lawsuits, and loss of card acceptance privileges. Completing your annual questionnaire eliminates the non-compliance charge — and the exposure — entirely.

Batch, Gateway, and Chargeback Fees

- Batch fees hit every time you close your daily transaction batch — small per-occurrence charges that accumulate across hundreds of batches annually

- Gateway fees cover online payment processing, billed monthly and/or per-transaction, often buried within larger line items

- Chargeback fees run $20–$100 per dispute, charged regardless of whether you win. Some processors (like Helcim) charge $15 only on lost disputes, but most charge win or lose

Early Termination and Auto-Renewal Fees

Many processing contracts include:

- Early termination fees typically run $295–$495 (U.S. Chamber of Commerce) — the FTC's case against First American Payment Systems involved a $495 cancellation fee

- Auto-renewal clauses roll contracts into new terms if you miss a cancellation window, locking you in for another full term with no warning

The FTC's 2022 action against First American Payment Systems — which resulted in a $4.9 million settlement — alleged hidden three-year contract obligations, surprise exit fees, and "zombie charges" that continued even after merchants revoked bank account authorization. Before signing any processing agreement, read the cancellation and auto-renewal clauses specifically — those are where the largest surprises tend to live.

Warning Signs Your Processor May Be Overcharging You

Your Effective Rate Is Higher Than Your Contract Rate

The effective rate formula is straightforward:

Total monthly processing fees ÷ Total monthly card sales volume × 100 = Effective rate %

Example: If you paid $1,800 in fees on $50,000 in card volume, your effective rate is 3.6%. If your quoted rate was 2.2%, that gap represents hidden charges — not volume fluctuation.

Credit card processing fees generally run 1.5%–3.5%, though Square estimates the average merchant discount rate at 2.87%–4.35%. If your effective rate sits at the top of that range or above it, an audit is warranted.

Monthly Fees Are Creeping Upward

Watch for gradual increases — new line items appearing, monthly charges ticking up by a few dollars, or per-transaction costs shifting slightly. Processors sometimes add or raise fees without written notice, which directly violates most standard agreement terms.

Statements Contain Vague Line Items

Specific terms to flag on any statement:

- "Misc. adjustment"

- "Non-qualified surcharge"

- "Funding fee"

- "Regulatory compliance fee"

- "Administrative fee"

None of these are self-explanatory. Each requires a mapped explanation tied to your original rate schedule. If your processor can't trace each charge back to your rate schedule, request a formal line-item breakdown in writing — and consider that a red flag during your next contract review.

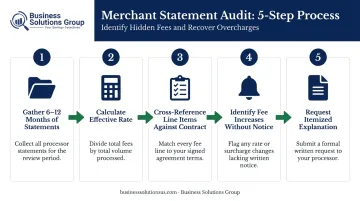

How to Audit Your Merchant Statements for Hidden Fees

Step 1 — Gather 6 to 12 Months of Statements

A single month won't reveal gradual fee creep. Fee increases tend to happen incrementally, and effective rates fluctuate month-to-month in ways that can mask a systemic overcharge. Reviewing a full year gives you a baseline and exposes trends.

Step 2 — Calculate Your Effective Rate

Run the formula for each month: total fees ÷ total card volume × 100. Then compare your effective rate against:

- Your quoted/contracted rate

- The general industry range (1.5%–3.5%, or 2.87%–4.35% per Square's data)

Consistent monthly gaps between quoted and effective rates confirm hidden fees are present.

Step 3 — Cross-Reference Every Line Item Against Your Contract

Pull your original merchant agreement and rate schedule. For every fee on your statement, find the corresponding line in the contract. Flag anything that:

- Doesn't appear in the contract at all

- Exceeds the contracted amount

- Has changed without a documented amendment

Step 4 — Identify Fee Increases Without Written Notice

Many processing contracts require advance written notification before rates can change. If fees increased without notice, this may constitute a breach of contract. Document every discrepancy with dates and amounts — this becomes your negotiation leverage.

Step 5 — Request an Itemized Explanation

You have the right to ask your processor for a complete breakdown of every fee on your statement. A legitimate processor will map each charge back to your contract clearly. Watch for these red flags in their response:

- Vague or non-specific explanations for a charge

- Resistance to providing a full fee breakdown

- Inability to connect a line item to your rate schedule

For businesses processing significant card volume, Business Solutions Group provides cost analysis services that benchmark your payment processing fees against market rates, identify overcharges, and surface margin that has been steadily lost to undisclosed fees.

Strategies to Reduce Hidden Processing Fees

Negotiate Directly With Your Processor

Many fees are negotiable, including monthly account fees, PCI compliance program fees, and the processor's markup. Competitive quotes from other processors serve as your strongest leverage — no processor wants to lose an established account over a $20/month service fee.

Switch to Interchange-Plus Pricing

Interchange-plus separates the actual interchange cost from the processor's markup on every statement line. You can see exactly what the network charges and exactly what the processor adds. That transparency makes overcharging far harder to hide and much easier to audit.

Optimize Transaction Data

For B2B merchants especially, passing complete transaction data reduces non-qualified surcharges. The more detail you submit per transaction, the lower the interchange tier — and the savings add up fast.

| Data Level | What It Includes | Visa Commercial Rate |

|---|---|---|

| Level 2 | Sales tax, customer PO number, merchant postal code | 2.50% + $0.10 |

| Level 3 | Adds line-item detail: quantity, product code, description, ship-to/from ZIP | 1.90% + $0.10 |

That 60-basis-point gap compounds quickly at scale. A merchant processing $500,000/year in commercial cards saves roughly $3,000 annually by qualifying at Level 3 instead of Level 2.

Calendar Your Contract Renewal Dates

Auto-renewal clauses are one of the most avoidable hidden costs in processing agreements. Set a calendar reminder 90 days before your contract end date. Use that window to:

- Request a full rate review

- Gather competitive quotes

- Renegotiate terms proactively — processors rarely offer improvements at renewal unless the merchant initiates the conversation

Frequently Asked Questions

Is it legal for merchants to charge a fee for credit or debit card payments?

In the U.S., merchants can generally add surcharges for credit card payments, subject to card network rules (Visa caps surcharges at 3% of the transaction; Mastercard at 4%) and state laws. At least 11 states, including Massachusetts, Connecticut, and Maine, prohibit credit card surcharges entirely. Debit card surcharges face stricter restrictions ; Mastercard prohibits them outright.

Why are merchants charging credit card processing fees?

Processing fees (interchange, assessment, and processor markup) come directly out of the merchant's margin. Surcharges and convenience fees shift some of that cost to the customer, particularly for businesses with thin margins where absorbing 2%–3.5% per transaction is operationally unsustainable.

How are merchants liable for credit card fraud?

Merchants without EMV chip-enabled terminals or PCI DSS compliance can be held financially liable for fraudulent transactions. Since the October 2015 liability shift, non-compliant merchants absorb counterfeit card fraud costs that would otherwise fall on the card network or issuer.

What is the average merchant credit card processing fee?

Effective rates typically fall between 1.5% and 3.5% for most card types, with rewards cards and non-qualified transactions pushing toward 2.87%–4.35% — often well above a merchant's quoted base rate.

How do I calculate my effective processing rate?

Divide your total monthly processing fees by your total monthly card sales volume, then multiply by 100. If you paid $900 in fees on $30,000 in card sales, your effective rate is 3.0%. Comparing this number to your quoted rate reveals the true cost gap.

What is interchange-plus pricing and why does it matter?

Interchange-plus separates the wholesale interchange cost from the processor's markup, showing both as distinct line items on your statement. This structure prevents processors from hiding inflated margins, unlike tiered pricing where downgrades and surcharges are bundled into opaque rate buckets.