Introduction

US merchants paid $187.20 billion in card processing fees in 2024, according to the Nilson Report. Credit card acceptance typically costs 1.5% to 3.5% of every transaction, per the Richmond Fed — meaning a business doing $1 million in annual card revenue hands over $15,000 to $35,000 a year in fees, often without a single line item getting a second look.

Those fees aren't fixed. They're the product of decisions — some made at setup, some made daily, some never revisited at all. The pricing model you chose, whether you negotiate your markup, how you submit transaction data, how fast you batch settlements — all of it compounds into your true effective rate over time.

This guide breaks down where those costs originate, which levers actually move the number, and what a systematic reduction strategy looks like — from initial pricing decisions through daily operational habits to the business context that shapes what's negotiable.

Key Takeaways

- Processing fees typically run 1.5%–3.5% per transaction, but your actual rate depends on factors you control

- Fees compound across three layers: interchange (non-negotiable), assessments (network fees), and processor markup (negotiable)

- Most businesses overpay due to poor setup decisions: the wrong pricing model, failure to negotiate, or an unfavorable card mix

- Operational habits around data submission, batch timing, and chargeback management directly raise or lower your effective rate

- Reducing fees means optimizing how you accept cards, not avoiding them

How Credit Card Processing Fees Accumulate Over Time

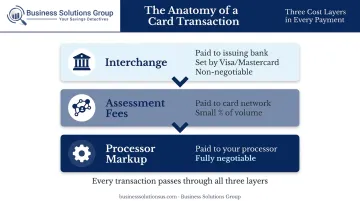

Most merchants see a single monthly total on their processing statement — but that number obscures a three-layer cost structure underneath it.

The Three Cost Layers

Every card transaction passes through:

- Interchange — paid to the card-issuing bank; set by Visa, Mastercard, and other networks; not negotiable by merchants

- Assessment fees — paid to the card network itself; typically a small percentage of volume

- Processor markup — your payment processor's fee on top; fully negotiable and highly variable by provider

Most processor statements don't break these layers out, so merchants rarely know what they're actually paying the processor versus what goes to the network. American Banker notes that tiered pricing makes this worse — grouping transactions into qualified, mid-qualified, and non-qualified buckets that obscure the real cost breakdown.

Why Costs Escalate Over Time

Costs don't stay static. They drift upward under specific conditions:

- Chargeback rate increases — triggers risk re-pricing by your processor

- More card-not-present transactions — online and keyed-entry payments carry higher interchange

- Increased rewards card acceptance — premium cards cost meaningfully more to accept

- Missing transaction data — incomplete data causes interchange downgrades to more expensive tiers

- Unchallenged junk fees — non-processing charges like PCI noncompliance fees and batch fees accumulate uncontested

Without monthly statement audits, fee creep goes undetected — sometimes for well over a year.

Key Cost Drivers for Credit Card Processing Fees

Understanding what drives your rate is the prerequisite to reducing it. Four factors account for most of the variability.

Card Type and Transaction Channel

Interchange rates vary dramatically by card type and how the transaction is processed. Current published schedules make this concrete:

| Transaction Type | Example Rate |

|---|---|

| Visa regulated debit (card-present) | 0.05% + $0.21 |

| Mastercard small-ticket (card-present) | 1.65% + $0.02 |

| Mastercard small-ticket (card-not-present) | 1.95% + $0.02 |

| Mastercard World Elite (rewards credit) | 2.30% + $0.10 |

| Visa commercial card (card-present) | 2.50% + $0.10 |

| Visa commercial card (card-not-present) | 2.70% + $0.10 |

| Mastercard/Visa non-qualified consumer credit | 3.15% + $0.10 |

Source: Visa 2026 Interchange Schedule, Mastercard 2025–2026 US Region Rates

A business with a high share of rewards credit cards or card-not-present transactions faces structurally higher costs than one running mostly in-person debit. Those costs aren't negotiable, but they are manageable once you understand where they come from.

Processor Markup

Unlike interchange, processor markup is fully negotiable. Businesses that accepted default rates at setup and never revisited them are often paying significantly above current market rates. This is the highest-ROI target for most merchants.

Data Quality and Qualification

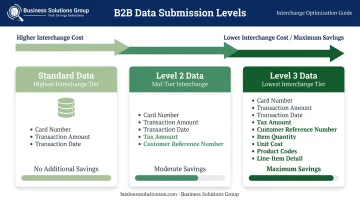

Incomplete transaction data causes downgrades, meaning your transaction gets reclassified into a more expensive interchange tier than it would otherwise qualify for. For B2B merchants accepting corporate or purchasing cards, Mastercard explicitly states that Level 2 and Level 3 data submission can reduce interchange costs.

Most businesses accepting these cards never configure it — and they pay more as a result.

Transaction Context

A B2B company accepting corporate cards has a fundamentally different cost profile than a retailer running mostly consumer debit. Knowing your own transaction mix — card types, channels, and average ticket sizes — tells you which of the strategies below will move the needle most.

Cost-Reduction Strategies for Credit Card Processing Fees

Effective strategies depend on where the excess cost originates. The framework below organizes interventions by leverage point.

Strategies That Reduce Costs by Changing Decisions

These target decisions made before or around processing: pricing model, processor selection, and payment policies.

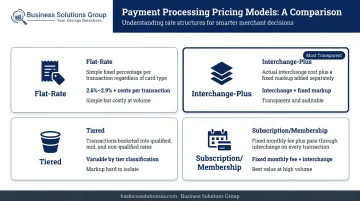

Choose the right pricing model. The four main models differ significantly in transparency and total cost:

- Flat-rate — simple, predictable, typically 2.6%–2.9% + fixed cents per transaction; often overpriced for higher-volume businesses

- Interchange-plus — your actual interchange cost plus a fixed processor markup; transparent and usually more cost-effective once volume justifies the statement complexity

- Tiered — buckets transactions into qualified/mid-qualified/non-qualified tiers; markup is hard to isolate, often hides processor margin

- Subscription/membership — fixed monthly fee plus pass-through interchange; can be cost-effective at high volume

The right model depends on your transaction volume, average ticket, and card mix. Run a break-even comparison using three months of actual statements before switching.

Negotiate your processor markup. Interchange is non-negotiable. Your processor's margin isn't. Come to that conversation with: your current effective rate (total fees ÷ total card volume), competitor quotes, your chargeback history, and your monthly processing volume. Businesses with stable revenue and low dispute rates have real leverage.

Shift large B2B payments to ACH. ACH bypasses interchange entirely. The AFP's 2022 Payments Cost Benchmarking Survey found an all-in median ACH cost of $0.26–$0.50 per item — versus percentage-based card fees that can reach 2%–3% on large invoices. For a $50,000 invoice, that's the difference between a $1,000+ card fee and a $0.50 ACH transaction.

Moving retainers, recurring invoices, and high-value receivables to ACH is one of the highest-impact, lowest-disruption changes available to B2B companies.

Set a minimum purchase threshold. US law (15 USC 1693o-2) permits merchants to require a minimum credit card purchase of up to $10, as long as it doesn't differentiate by issuer or card network. On a $3 transaction, a 2.5% fee represents a meaningful margin erosion. The minimum policy solves it without turning away customers.

Strategies That Reduce Costs by Changing How Processing Is Managed

These are operational habits — not one-time changes, but ongoing practices that add up over time.

Run a monthly statement audit. Most processors charge non-processing fees that appear as line items merchants rarely scrutinize: PCI noncompliance fees, monthly minimums, gateway fees, batch fees, statement fees. Pull a full statement and categorize every fee by type. Fees that can't be explained or justified are candidates for removal or negotiation.

Submit Level 2 and Level 3 data for B2B transactions. For businesses accepting corporate, purchasing, or government cards, this is one of the most underused cost levers available. Level 2 data adds tax amount and customer reference numbers. Level 3 adds line-item detail. Both move transactions into lower-cost interchange tiers. This requires a compatible payment gateway — your processor can confirm compatibility.

Use AVS/CVV verification and batch daily. Address verification and CVV checks reduce fraud signals on card-not-present transactions, which can affect qualification. On settlement timing: Mastercard requires certain Payment Transactions to be presented within one calendar day, no later than 24 hours after authorization. Visa recommends settling within 1–5 days of the transaction date. Late presentment creates chargeback risk and potential qualification downgrades.

Manage chargebacks actively. Disputes carry per-incident fees (the US Chamber cites a typical range of $20–$100 per dispute — verify your own contract terms). A rising chargeback rate signals elevated risk to your processor, which can trigger broader rate increases.

Visa's VAMP program sets an excessive threshold at 220 basis points, dropping to 150 bps in April 2026. Key prevention levers:

- Clear, recognizable billing descriptors

- Strong refund and return policies

- Fraud filters on card-not-present transactions

- A defined workflow for responding to disputes within required windows

Strategies That Reduce Costs by Changing the Context Around Processing

Broader context matters too — the payment channel, who absorbs the fee, and whether your current rates have ever been benchmarked against market standards.

Prioritize card-present transactions. In-person chip and tap payments carry lower interchange than online or keyed-entry transactions — the rate differential between card-present and card-not-present can be 0.30% or more on the same card type. Businesses currently processing a significant share of phone orders or manually keyed payments should evaluate whether some of those transactions could convert to in-person or QR code payments.

Implement a surcharge or cash discount program. Surcharges pass the processing fee directly to card-paying customers — capped at the merchant's actual acceptance cost or 3%, whichever is lower, per Visa's rules. Cash discount programs offer a reduced price for non-card payment. Both shift the cost burden, but both require careful implementation:

- Debit and prepaid cards cannot be surcharged under Visa network rules

- Credit card surcharges are prohibited in Connecticut, Massachusetts, and Puerto Rico; other states have varying disclosure requirements

- Proper disclosure at checkout is required under card network rules

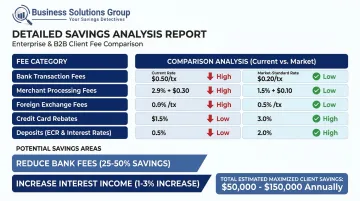

Apply structured cost benchmarking. Many businesses don't know their blended effective rate — or how it compares to others with a similar transaction profile and industry. A structured benchmarking analysis compares your actual rates and fees against market standards for your transaction type, average ticket size, and industry — flagging hidden markups, misclassified interchange categories, and outdated pricing structures.

Business Solutions Group offers this as a no-cost Detailed Savings Analysis Report, delivered as a side-by-side comparison with no obligation to proceed. For enterprise and B2B clients, even a 0.1%–0.2% reduction in effective rate can translate into tens of thousands of dollars in annual savings.

Conclusion

Credit card processing fees respond to specific, identifiable interventions — not generic cost-cutting. The reduction opportunity sits across three layers: decisions made at setup (pricing model, processor choice, payment policies), operational habits maintained daily (data quality, settlement timing, dispute management), and the external context around each transaction (channel, card mix, surcharging).

None of these is a one-time fix. Staying ahead of processing costs requires ongoing attention across each layer:

- Pricing models need annual reviews as transaction volume and mix change

- Statement audits should become a routine line item, not a reactive exercise

- Operational practices around data submission and fraud prevention build measurable savings over time

Businesses that consistently pay less for payment acceptance treat their effective rate as a managed metric. That shift in mindset — from fixed cost to controllable variable — is where the real savings compound.

Frequently Asked Questions

How do I lower my credit card processing fees?

Start by calculating your effective rate (total monthly fees ÷ total card volume), then audit your statement for non-processing fees. Negotiate your processor markup, ensure you're on the right pricing model for your volume, and reduce chargebacks. Each lever addresses a different cost layer.

Is it legal to charge a 3% credit card fee?

Credit card surcharges are legal in most US states but prohibited in Connecticut, Massachusetts, and Puerto Rico. Surcharges must be disclosed at checkout and capped at your actual acceptance cost or 3%, whichever is lower. They cannot be applied to debit or prepaid cards under Visa network rules.

Is a 3% credit card processing fee high?

It sits at the upper end of the typical 1.5%–3.5% range. A 3% rate is common for rewards cards, card-not-present transactions, or flat-rate pricing. Switching to interchange-plus pricing and submitting Level 2/3 data for B2B transactions can bring effective rates well below that range.

What is the cheapest way to accept credit card payments?

The lowest-cost combination is interchange-plus or subscription pricing, card-present transactions (chip/tap), and ACH for large or recurring B2B invoices. The optimal mix depends on your transaction volume, average ticket size, and card type distribution.

Can I negotiate credit card processing fees?

Yes, though only the processor markup is negotiable. Interchange and assessment fees are set by card networks and cannot be changed. Your leverage increases with higher monthly volume, low chargeback rates, and competing quotes from other providers.

What is interchange-plus pricing and is it better for small businesses?

Interchange-plus charges the actual interchange rate plus a fixed processor markup, making costs transparent and auditable. It benefits businesses with enough volume to manage statement complexity. For very small or seasonal businesses, flat-rate pricing offers more predictable monthly costs.