The core problem isn't that processing fees are inherently expensive. It's that opaque pricing structures, passive acceptance of incremental rate increases, and a lack of regular oversight turn a manageable cost into a compounding one. Most businesses never calculate their true effective rate or scrutinize their monthly statements closely enough to catch the drift.

This post walks through how fees accumulate, what actually drives them, and a structured five-step audit process — followed by the specific strategies that reduce costs without disrupting operations.

Key Takeaways

- Processing fees include interchange, assessments, and processor markups — only the markup layer is negotiable

- Most businesses overpay because they never calculate their effective rate or audit for hidden fees

- A structured audit means gathering statements, categorizing fees, calculating your effective rate, and benchmarking against industry averages

- The highest-impact moves are switching to interchange-plus pricing, eliminating junk fees, and renegotiating processor markups

- Monthly monitoring prevents processors from incrementally raising rates without notice

How Payment Processing Fees Typically Build Up

Processing fees rarely appear as a single clean line item. They accumulate across multiple categories and are presented in ways that make the true total difficult to calculate without deliberate effort:

- Interchange fees

- Assessment fees

- Payment gateway fees

- Processor markups

- Monthly minimums

- PCI compliance fees

- IRS reporting fees

That difficulty is exactly what makes the build-up so effective. Processors may raise rates slightly multiple times per year, add new administrative fees, or reclassify transactions to higher-cost tiers. Processors bury these changes in dense monthly statements that most businesses file without close review.

The FTC has charged and settled with payment processing marketers specifically for deceiving small businesses through low advertised rates and hidden or fine-print fees — a sign of how deliberately confusing this cost category can be.

The real cost only surfaces when you calculate your effective rate. A business processing $50,000 per month won't immediately notice a 0.2% rate increase on a dense statement — but over 12 months, that's $1,200 in unnecessary spend. At $500,000 per month, that same overlooked adjustment costs $12,000 annually.

Key Cost Drivers for Payment Processing Fees

Understanding what drives costs tells you where you actually have leverage — and where you don't.

The Three-Layer Cost Structure

| Layer | What It Is | Negotiable? |

|---|---|---|

| Interchange | Fees set by card networks (Visa, Mastercard), passed to card-issuing banks | No — but optimizable |

| Assessments | Fixed network charges (e.g., Visa charges 0.14% on credit, Mastercard 0.13%) | No |

| Processor markup | The processor's margin added on top of interchange and assessments | Yes — fully negotiable |

According to a Federal Reserve analysis, interchange alone accounts for 70–90% of total credit card processing cost. That's the floor you can't negotiate away — but it's one you can optimize.

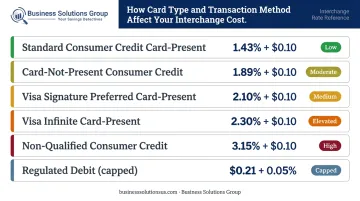

How Card Type and Transaction Method Shift Costs

The specific cards your customers use and how transactions are processed affect your interchange cost:

- Standard consumer credit, card-present retail (Visa): 1.43% + $0.10

- Visa Signature Preferred (rewards), card-present: 2.10% + $0.10

- Visa Infinite (premium rewards), card-present: 2.30% + $0.10

- Card-not-present consumer credit (Visa): 1.89% + $0.10

- Non-qualified consumer credit (Visa): 3.15% + $0.10

- Regulated debit (Federal Reserve cap): $0.21 + 0.05%

Premium rewards cards, card-not-present transactions, and manually keyed entries carry significantly higher interchange rates — sometimes 2x the cost of standard card-present transactions than standard debit or card-present transactions. Your card mix matters.

Internal Decisions That Drive Cost

Several cost drivers are entirely within your control:

- Which pricing model you accepted (tiered vs. interchange-plus vs. flat-rate)

- Whether PCI compliance is maintained (non-compliance fees are pure overhead)

- Whether transaction data is submitted accurately and within required timeframes

- Whether your pricing model aligns with your transaction volume and card mix

Unlike interchange rates, these factors respond directly to how you operate. Fixing even one can move the needle on your effective rate.

How to Audit Your Payment Processing Fees

Step 1: Gather Your Statements and Agreement

Pull 6–12 months of merchant statements, your processing agreement, and any fee schedules from your processor. A multi-month window is necessary — it reveals pattern changes, irregular charges, and gradual rate creep that a single month hides.

Step 2: Categorize Every Fee

Go line by line and sort each fee into one of these buckets:

- Interchange passthrough — fees passed from card networks to card issuers

- Assessment fees — fixed network charges (Visa, Mastercard)

- Processor markup — the processor's added margin

- Miscellaneous fees — statement fees, PCI non-compliance fees, IRS reporting fees, regulatory fees, monthly minimums, batch fees

Flag any fee you cannot clearly explain. If you can't define it, it may be negotiable or removable.

Step 3: Calculate Your Effective Rate

This single calculation cuts through all pricing complexity:

Effective Rate = (Total Fees Charged ÷ Total Sales Volume) × 100

If you paid $4,500 in fees on $150,000 in sales, your effective rate is 3.0%.

The Federal Reserve reports that average credit card processing fees range from 1.5% to 3% of transaction value. A rate at the top of that range — or above it — is worth investigating. This is especially true if your card mix includes significant regulated debit volume, which carries far lower interchange costs.

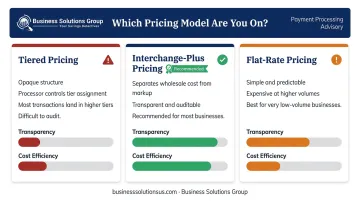

Step 4: Evaluate Your Pricing Model

Your pricing model determines whether you even have the visibility to audit accurately:

- Tiered pricing — bundles transactions into "qualified," "mid-qualified," and "non-qualified" tiers. Opaque by design; processors control which tier each transaction falls into, and most end up in higher tiers than merchants realize.

- Interchange-plus pricing — separates the actual interchange cost from the processor's markup. Transparent and auditable.

- Flat-rate pricing — simple and predictable, but typically expensive at higher volumes. Appropriate for very low-volume businesses.

If you're on tiered pricing, the structure itself is the problem — you can't get a complete picture of your costs without switching models.

Step 5: Review for Transaction Downgrades

Once you understand your pricing model, look for downgrades — transactions that fail to meet qualification criteria and get reclassified into a higher-cost interchange category. Common causes include:

- Missing transaction data (especially for commercial cards)

- Batch settlement delays beyond 24 hours

- Card-not-present transactions missing proper authorization codes

- Incorrect transaction type classification

Downgrades inflate your costs without any clear label. They don't appear as a "downgrade fee" line item — they show up as higher interchange charges that blend in unless you're comparing expected vs. actual interchange categories.

Cost-Reduction Strategies for Payment Processing Fees

Not all cost-reduction moves carry equal weight. Some require a one-time structural change; others require ongoing operational discipline. Below are the highest-impact approaches, grouped by what you need to change.

Strategies That Change the Structure

Switch to interchange-plus pricing. This is the single most impactful structural decision. It separates the non-negotiable wholesale cost from the processor's margin, making future audits easier and limiting the processor's ability to inflate fees invisibly. If you're on tiered pricing, requesting a repricing to interchange-plus is the first call to make.

Renegotiate processor markups. Processor markups are always negotiable — particularly if you have 6+ months of volume data. Higher processing volumes provide leverage, and benchmarking your rates against market standards gives you a credible basis for the conversation. Many businesses that request a review receive better terms without changing processors.

Eliminate junk fees at contract review. Common fees that are often removable:

- Statement fees

- IRS reporting fees

- "Regulatory compliance" fees

- Next-day funding fees

- Batch fees

Many of these exist because processors add them knowing most merchants don't scrutinize statements. Asking directly for their removal frequently works.

Evaluate card acceptance policies. Setting minimum transaction thresholds for credit cards, prioritizing debit acceptance for low-margin transactions, and reducing card-not-present volume where possible all reduce the proportion of high-cost transactions in your mix.

Strategies That Improve Operational Control

Submit Level 2 and Level 3 transaction data. For businesses accepting commercial, purchasing, or corporate cards, submitting enriched transaction data — tax amount, purchase order number, line-item detail — qualifies transactions for lower interchange categories. This requires processor and software support, but for B2B companies with significant commercial card volume, it's one of the most effective cost-reduction steps available.

Prevent downgrades through process discipline:

- Batch transactions within 24 hours of authorization

- Ensure card-present transactions are processed correctly at the terminal

- Use address verification (AVS) consistently on card-not-present transactions

Monitor the effective rate monthly. Recalculate your effective rate each month and flag any upward movement. This isn't a one-time audit — it's a management habit. Processors may adjust rates semiannually; catching a 0.1% increase in month two prevents paying it for the next 10 months.

Maintain PCI compliance. PCI non-compliance fees are avoidable overhead. Completing the annual self-assessment questionnaire (SAQ) (the primary compliance mechanism for most small and mid-size businesses) eliminates these charges entirely. One processor's disclosed fee for non-compliance is $29.95/month; others charge more.

Strategies That Change the Context Around Processing

Implement a surcharge or cash discount program. Surcharging adds a fee to credit card transactions; cash discounting sets a higher list price with a reduction for non-card payment. Both are legal mechanisms to offset processing costs, but rules apply:

- Visa caps surcharges at 3%; Mastercard caps them at the merchant's average discount rate with a 4% absolute maximum

- Both networks require 30 days' notice before surcharging begins

- Surcharging is prohibited on debit and prepaid cards

- Connecticut, Maine, Massachusetts, and Oklahoma restrict or prohibit surcharging — check current state law before implementing

Consolidate processing relationships. Businesses operating multiple locations or processing through multiple vendors often pay higher per-unit costs and redundant technology fees. Consolidating under a single processor agreement creates volume leverage for negotiation and simplifies oversight. This is particularly relevant for logistics and multi-site operations where fragmented setups are common.

Benchmark fees against industry standards. Without an external benchmark, there's no way to know whether your effective rate is competitive or simply familiar. Business Solutions Group's spend intelligence approach addresses this gap directly: a no-cost, line-by-line analysis of merchant statements that benchmarks your actual rates against what comparable businesses in your industry and transaction profile are paying.

The analysis surfaces hidden markups, interchange categorization issues, pricing model misalignments, and avoidable fees that internal reviews typically miss. Clients typically see 25–35% in potential savings identified — with no commitment required to proceed.

Conclusion

Payment processing fees become expensive through passive acceptance and lack of oversight — not because the cost is inherently fixed. The businesses that manage this category most effectively treat it as an ongoing operational discipline: calculating the effective rate monthly, reviewing statements for new fees, and auditing at least quarterly.

The audit process is the foundation. Without knowing your effective rate, your pricing model, and where fees are accumulating, any reduction effort is guesswork. Build the audit into your regular financial review cycle — most businesses that do this consistently find the savings in year two exceed those in year one, simply because the review becomes more targeted over time.

Frequently Asked Questions

Is a 3% payment processing fee high?

The Federal Reserve reports that average credit card processing fees range from 1.5% to 3% of transaction value , so 3% sits at the top of that range. Whether it signals overpayment depends on your card mix, transaction channel, and pricing model. A business with high regulated debit volume at 3% is almost certainly overpaying; one with a premium rewards card-heavy mix may be closer to average.

What is a reasonable fee for a payment processing fee audit?

Many audits are offered at no cost by third-party consultants who work on a performance or savings-share basis. Business Solutions Group, for example, provides a no-cost, no-commitment benchmark analysis that identifies potential savings before any implementation decisions are made. Paid independent audits vary in price by volume, complexity, and scope — no standard market rate applies.

What types of audits are used to review payment processing fees?

Three main approaches exist:

- Self-conducted audits: Review statements independently using effective rate calculations

- Third-party independent audits: Conducted by consultants with no processor affiliation

- Processor-initiated reviews: Carry an inherent conflict of interest; processors have limited incentive to surface their own overcharges

Can you pass payment processing fees to customers?

Yes, through compliant surcharge programs (credit card transactions only) or cash discount programs. Surcharging rules vary: Visa caps surcharges at 3%, Mastercard at 4%, and both require 30 days' advance notice. Several states restrict surcharging, so verify current state law before implementing either program.

What is an effective rate in payment processing, and how do I calculate it?

The effective rate is the true percentage of total sales paid in processing fees: (total fees ÷ total sales volume) × 100. It's the most reliable single metric for comparing actual costs across processors or time periods — far more useful than quoted rates alone.

How often should businesses audit their payment processing fees?

Review the effective rate monthly to catch rate increases early. Conduct a thorough formal audit (categorizing all fees, evaluating the pricing model, and reviewing for downgrades) at least quarterly — more often for high-volume or multi-location businesses.