Introduction

Most logistics managers assume their carrier discounts are competitive because the carrier said so at signing. That assumption is expensive.

UPS and FedEx apply annual General Rate Increases (GRIs) of roughly 5.9% per year, compounding to approximately 32% cumulative base rate inflation from 2022 through 2026. According to ZDS Consulting, companies routinely overpay for shipping by 15–30% due to complex, non-transparent pricing structures.

Yet most shippers renegotiate carrier contracts infrequently, if ever.

Parcel shipping contract benchmarking is the structured process of comparing your carrier agreement's rates, fees, and terms against what comparable businesses are actually paying in today's market. It's one of the highest-impact levers available for reducing transportation costs — and consistently one of the least used.

This guide breaks down the full benchmarking process: what to compare, where shippers typically leave money on the table, and how to use the data to negotiate from a position of strength.

Key Takeaways

- Benchmarking measures your carrier rates, surcharges, and contract terms against real market data from shippers with a matching profile — not published list prices or carrier-supplied quotes

- The biggest savings are typically hidden in accessorial fees and surcharges, which now represent 20–40% of total parcel spend for many shippers

- Accurate benchmarking requires at least 12 months of transaction-level invoice data — actual billed amounts pulled from carrier invoices, not quoted rates

- Annual GRIs erode contract value fast; a deal that looked competitive at signing can be above market within 12–18 months

- Comparing your contract to a shipper with a different volume, zone mix, or service profile will skew results and lead to the wrong conclusions

What Is Parcel Shipping Contract Benchmarking?

Parcel shipping contract benchmarking is a structured evaluation of your carrier agreement's rates, incentives, and terms against what the market currently offers businesses with a comparable shipping profile. Comparable means similar volume, package characteristics, service mix, and geography.

The goal isn't simply to know whether your rates look high. It's to identify cost gaps with enough precision to build a fact-based negotiation strategy, rather than walking into a carrier conversation with nothing but a request for better pricing.

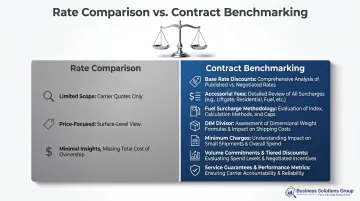

How It Differs from a Rate Comparison

A rate comparison is a one-dimensional exercise: you solicit quotes from carriers and compare the numbers. Benchmarking is different in scope.

A complete benchmark evaluates:

- Base rate discounts and tier structure

- Accessorial fees (residential, delivery area, additional handling, address correction)

- Fuel surcharge index methodology and current rate level

- Dimensional (DIM) weight divisor

- Minimum per-package charges

- Volume commitment thresholds and penalty structures

- Service-level guarantees and carrier compliance metrics

Rate comparisons show what a carrier is willing to offer. Benchmarking shows what similar businesses are actually paying — and that gap is where most negotiating leverage lives.

Why Parcel Shippers Need Contract Benchmarking

Carriers Have a Structural Data Advantage

Carriers like UPS and FedEx control over 80% of the U.S. parcel market and maintain sophisticated pricing models built on data from millions of shippers. Most businesses, by contrast, renegotiate contracts infrequently and without access to peer pricing data.

Sifted puts it plainly: carriers "possess far more data than the shippers they serve" and use pricing models "that shippers cannot easily replicate without external data." Shipware estimates 9 out of 10 shippers overspend as a result.

Benchmarking closes that gap. Business Solutions Group, for example, maintains visibility into thousands of pricing agreements and employs former UPS and FedEx senior-level pricing analysts — giving shippers access to the same market intelligence carriers use when setting rates.

The Discount Number Is Misleading on Its Own

Many shippers treat the headline discount percentage as the primary measure of contract quality. This leads to real blind spots.

According to industry data, accessorial fees and surcharges now represent 20–40% of total parcel spend for most shippers — a figure that has climbed steadily over five years and can reach 40% during peak season. A high base discount paired with above-market accessorial fees frequently produces a worse total cost than a lower discount with competitive fee structures.

GRIs Erode Contract Value Faster Than Most Shippers Realize

Both UPS and FedEx have applied GRIs of 5.9% annually (with a spike to 6.9% in 2023, the largest in FedEx's history). Compounded from 2022 to 2026, that's roughly 32% cumulative base rate inflation.

The headline percentage actually understates the problem. As Brad McBride of ZDS/ShipSigma noted, actual shipping costs are "likely up 8–12%" in most years because most surcharges climb 6–7% independently of the headline GRI. A contract competitive at signing can become materially above market within 12–18 months.

Benchmarking Shifts the Negotiation Dynamic

That rate of erosion is exactly why benchmarking matters at the negotiating table. Without market data, the carrier conversation sounds like: "We'd like better rates." With benchmarking, it becomes: "Our residential surcharge is $X above what comparable shippers pay — here's the line-item gap." Carriers respond to specifics. Business Solutions Group clients typically achieve 20–25% net savings on parcel spend through benchmarking-informed renegotiation.

How the Benchmarking Process Works

The process moves through three sequential phases: building an accurate internal shipping profile, comparing it against market data from similar shippers, and translating the gap analysis into a negotiation strategy.

Step 1: Gather and Normalize Your Shipping Data

The starting point is compiling at least 12 months of shipment-level data, including:

- Package weights and dimensions

- Origin and destination ZIP codes

- Service types used (Ground, 2-Day, Overnight, etc.)

- Zone distribution

- Full breakdown of accessorial fees actually charged

Transaction-level invoice data — what was actually billed and paid — is more reliable than quoted or contracted rates, which regularly diverge from real-world costs once carriers apply surcharges and minimums.

Spend intelligence tools or freight audit platforms make this stage significantly faster by normalizing complex carrier invoice data into a structured, analysis-ready dataset. Business Solutions Group, for example, aggregates and structures parcel invoice data across UPS, FedEx, and regional carriers — with a full analysis phase that typically takes about one week.

Step 2: Compare Against Market Benchmarks

The comparison phase requires access to real, aggregated transaction data from shippers with a similar profile. Two data sources that don't qualify:

- General industry price indexes — these reflect list prices, not negotiated rates

- Fresh carrier quotes — these show what a carrier is willing to offer today, not what the market is paying

The benchmark must be profile-specific. A shipper with 80% residential delivery in remote ZIP codes has a fundamentally different cost profile than one delivering primarily to commercial addresses in dense metro areas. Comparing those two contracts against each other produces misleading conclusions.

That profile distinction also applies to your data source selection. Internal benchmarking — comparing performance across your own divisions or distribution centers — can surface operational inefficiencies. But only external competitive benchmarking against peers provides the market context required for carrier negotiations.

Step 3: Identify Gaps and Build a Negotiation Strategy

The output of the comparison phase is a gap analysis that quantifies, line item by line item, where your rates, fees, and terms fall above or below market for your profile.

This translates directly into a prioritized negotiation target list. Common high-impact items include:

- Residential surcharge discount or cap

- Fuel surcharge index provision or ceiling

- DIM weight divisor

- Minimum charge structure

- Delivery area surcharge (DAS) tiers

This step should also incorporate carrier performance data — on-time delivery rates, invoice accuracy, damage frequency. The lowest rate from a carrier with chronic service failures isn't a good deal. The benchmark should reflect total contract value, not just pricing.

Key Elements to Benchmark in a Parcel Contract

Base Rate Discounts and Tier Structure

Most carriers structure discounts in tiers based on weekly or annual spend commitments. What qualifies as competitive varies significantly depending on shipping volume, service mix, and your credible leverage to shift volume to a competing carrier.

General directional guidance: advisory firms suggest standard contracts typically land 10–25% off published rates, while high-volume shippers with strong negotiating positions can achieve 30–40% or more. These figures are directional — the only reliable benchmark is profile-specific peer data, not published ranges.

Accessorial Fees

Base rate discounts often get the most attention in negotiations, but accessorial fees are where contracts most commonly drift above market without shippers noticing. Current 2026 per-package rates illustrate the stakes:

| Charge | UPS | FedEx |

|---|---|---|

| Residential Delivery Surcharge | $6.50 | $6.45 |

| DAS Ground Residential | $6.55 | $6.10 |

| DAS Ground Residential Extended | $8.85 | $7.70 |

| Address Correction | $25.25 | $22.50–$24.00 |

At scale, these per-package charges compound fast. A shipper sending 5,000 residential packages per week with an above-market residential surcharge of just $0.50 per package loses $130,000 annually on that single line item alone. High-volume shippers can typically negotiate percentage discounts or caps on accessorial categories — but only if they know where they stand relative to market.

Fuel Surcharge Mechanism

As of May 2026, UPS Ground fuel surcharge stands at 27.75% and Domestic Air at 30.75%. Both carriers update surcharges weekly based on EIA energy indices.

The specific percentage applied at a given fuel price tier differs between UPS and FedEx, meaning two otherwise identical contracts can produce different effective costs depending on which carrier's index formula applies. Contracts that lack fuel surcharge caps or alternative index provisions expose shippers to uncapped cost increases.

Business Solutions Group's data shows the UPS Domestic Ground fuel surcharge has risen 24.3% since January 2025 based on the underlying index movement. Without renegotiation protection, that cost flows directly to shippers.

Dimensional (DIM) Weight Pricing

Both UPS and FedEx use a standard DIM divisor of 139 for domestic parcel shipments. The formula: (L × W × H) ÷ 139 = DIM weight in pounds. Carriers bill whichever is greater: actual weight or DIM weight.

The divisor is negotiable. Key benchmarks to know:

- Moving from 139 to 166 reduces DIM weight charges by more than 16% for affected packages

- Shippers with sufficient volume can negotiate to 166 or even 194

- E-commerce businesses with lightweight, bulky packaging typically see the highest impact from this single line item

For businesses where DIM weight regularly exceeds actual weight, the divisor can be one of the highest-value items in the entire contract negotiation.

Minimum Charges and Volume Commitments

Minimum per-package charges create a billing floor for lightweight shipments, frequently set well above the calculated rate. Volume commitment thresholds, if unrealistically high, can trigger penalties that erase negotiated savings entirely.

Benchmark both against your actual shipping patterns and your projected volume over the contract term. Commitments that look reasonable at signing can become liabilities as your business changes.

Common Misconceptions in Parcel Benchmarking

"We can benchmark by comparing our contract to what another shipper pays."

Carrier pricing is highly specific to package characteristics, delivery density, zone distribution, and service mix — so comparing your agreement to another company's contract is unreliable. Two businesses spending identical annual amounts with UPS can receive very different pricing because their packages carry different cost profiles for the carrier.

Effective benchmarking compares your contract to what the market offers for shippers with your specific characteristics.

"The base discount is the most important number." Focusing on the headline discount leads shippers to overlook surcharges and accessorials that represent 20–40% of total spend. A high base discount paired with above-market accessorial fees frequently produces worse total cost than a lower discount with competitive fee structures across the board.

"We benchmarked at contract signing — we're covered." Annual GRIs, new surcharge introductions, and changes in your own shipping profile mean a benchmark can become stale within 12–18 months. Ongoing cost monitoring catches creep early and informs tactical decisions throughout the contract term, not just at renewal.

"Carrier quotes are a reliable benchmark." Quotes reflect what a carrier is willing to offer — not what the market is actually paying. Real benchmarking requires transaction data from comparable shippers. That's why advisory firms with broad market databases consistently produce more accurate benchmarks than soliciting quotes during an active negotiation.

Recognizing these misconceptions is the first step — the next is understanding what a rigorous benchmarking process actually looks like.

Frequently Asked Questions

What is a benchmark in a contract?

A benchmark is a reference point used to evaluate whether agreed-upon rates, terms, or service levels are competitive relative to current market conditions for comparable buyers. In parcel shipping, this means comparing your negotiated carrier rates and fees against what similarly profiled shippers are actually paying.

What are the 4 pillars of contract management?

The four pillars are contract creation, compliance monitoring, performance management, and renewal/renegotiation. Benchmarking directly supports performance management and renegotiation, making it a cross-functional tool across at least two of the four.

What data do I need to benchmark my parcel shipping contract?

You'll need at minimum 12 months of transaction-level invoice data: package weights, dimensions, origin/destination ZIP codes, service types, zone distribution, and a full accessorial fee breakdown. Actual billed amounts are more reliable than contracted or quoted rates.

How often should I benchmark my parcel shipping contract?

A deep-dive analysis should occur at minimum annually, ideally 6–12 months before contract renewal. Ongoing monitoring should be continuous — GRIs, new surcharges, and shifts in your shipping profile can erode a competitive contract within a year or two.

What is the difference between benchmarking and a rate comparison?

A rate comparison is narrow and price-focused — getting quotes from carriers and comparing numbers. Benchmarking is a comprehensive evaluation of your total cost structure: accessorial fees, fuel surcharge formulas, DIM factors, and service-level guarantees, all measured against market data from similarly profiled shippers.

Can small businesses benefit from contract benchmarking?

Yes, though the methodology and potential savings scale with spend volume. Lower-volume shippers may focus on fewer variables — key lanes and highest-frequency surcharges. A third-party advisor with access to broad market data can close that gap. Business Solutions Group, for example, works with shippers starting at 500 packages per month, giving smaller businesses benchmarking intelligence they couldn't generate on their own.