Introduction

Most shippers think they understand their shipping costs. They see the base rate, they know the carrier, and they assume the contract they signed is still working for them. It isn't.

Carrier rate increases don't stop at the headline GRI figure. According to Shipware, "very few shippers will realize an increase equivalent to 5.9%; most will be higher" — because surcharges, new fee categories, and contract escalators layer on top of the base rate increase, compounding the total increase.

Parcel spend is one of the largest controllable costs for most shippers. And the businesses that treat it that way — auditing regularly, negotiating aggressively, and benchmarking against the market — consistently outperform those that leave it on autopilot. Heading into 2026, that gap is widening.

This guide covers five concrete strategies for parcel contract optimization: mapping your shipping profile, auditing surcharges systematically, negotiating with benchmark data, diversifying your carrier mix, and building optimization into a year-round practice — with actionable steps for small parcel shippers, freight teams, and procurement managers.

Key Takeaways

- Audit your shipping profile first: volume, zones, weights, service levels, and surcharge exposure all shape what you should be negotiating

- Surcharges aren't an afterthought: at 25–40% of total parcel spend, they're your highest-leverage negotiation target

- Benchmark data changes the conversation — when you know what comparable shippers pay, the carrier's standard offer becomes indefensible

- Carrier diversification breaks lock-in: regional carriers run 10–40% cheaper on specific lanes and shipment types

- One-time optimization is a losing strategy — contracts erode on a schedule; your renegotiation cadence should too

Why Parcel Contract Optimization Is Non-Negotiable in 2026

Three consecutive years. That's how long UPS and FedEx have delivered 5.9% General Rate Increases — in 2024, 2025, and again for 2026. For a shipper who hasn't renegotiated since 2023, the cumulative compounding effect on base rates alone is substantial — and that's before accounting for surcharge increases, which routinely outpace the headline GRI.

Meanwhile, parcel volume keeps climbing. The Pitney Bowes Parcel Shipping Index reported US parcel volume reached 22.4 billion shipments in 2024 — a 3.4% increase year-over-year — with projections of 30.5 billion shipments by 2030. More volume means greater carrier dependency, which weakens negotiating leverage unless you come prepared.

For most companies that haven't independently benchmarked their parcel contracts in the last two to three years, overpaying is the default — often without knowing it. Business Solutions Group's client data puts that figure in the 15–30% range, with savings opportunities averaging 23.6% for clients who engage in active contract optimization.

Left unreviewed, contracts auto-renew on carrier-favorable terms. Every year without renegotiation is another year of compounding exposure:

- GRIs applied directly to your base rates

- New surcharge categories added without notice

- DIM divisors adjusted in carriers' favor

- Minimum charge thresholds quietly raised

Strategy 1: Map Your Full Shipping Profile Before Touching the Contract

What a Shipping Profile Actually Is

A shipping profile is a complete, data-driven picture of how your business ships: total parcel volume by month and season, service levels used (Ground, 2-Day, Overnight), average package weights and dimensions, zone distribution, and the surcharges most frequently applied to your shipments.

Every strategy in this guide builds on it — skip this step and your contract negotiation starts at a disadvantage.

How to Build One

Pull 12 months of invoice data and categorize spend by:

- Service type (Ground vs. express vs. overnight)

- Fee type (line-haul, fuel surcharge, residential, DAS, additional handling, etc.)

- Zone distribution (zones 2–4 vs. 5–8)

- Seasonal patterns (volume spikes that affect peak surcharge exposure)

The goal is to identify patterns your carrier already knows about — and that you should too. For example, if 60% of your shipments go to zones 2–4, that fundamentally reshapes the rate conversation. Carriers price against shipper behavior; knowing your own patterns better than the rep across the table shifts the negotiation in your favor from the first meeting.

What Most Shippers Miss

The biggest blind spot in shipping profile analysis is accessorial fees. Most teams focus on line-haul costs and treat surcharges as background noise. They shouldn't.

Industry data from FreightWise puts accessorials at 25–40% of total package shipping cost. During peak seasons or for unmanaged shipping profiles, that figure can climb higher. Sifted's own client data shows 36% of total shipping spend goes to accessorial fees across their base.

Spend analysis alone isn't enough, though. Your shipping profile should also surface carrier performance gaps — late deliveries, claim rates, and service failures. Documented SLA failures give you grounds for renegotiation mid-contract, and carriers take those conversations seriously when the data is in front of them.

Strategy 2: Audit Hidden Fees and Surcharges Systematically

The Surcharges Worth Your Attention

"Hidden" is a strong word — these fees are technically disclosed. But they're buried in invoice addenda and contract appendices in ways that make it easy to underestimate their total cost. The main categories to audit:

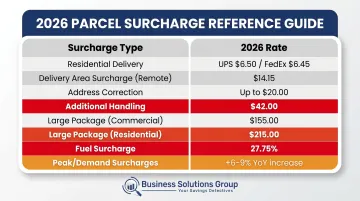

- Residential delivery surcharge — UPS charges $6.50 per package in 2026; FedEx charges $6.45

- Delivery Area Surcharge (DAS) — applies to rural and remote ZIP codes; UPS expanded its DAS ZIP code list, pushing the remote surcharge from ~$4.90 to $14.15 for affected destinations

- Address correction fees — can exceed $20 per shipment

- Additional handling — $42.00 per package for weight-based triggers

- Large package surcharge — $155.00 commercial, $215.00 residential

- Fuel surcharges — UPS's domestic ground surcharge was 27.75% as of May 2026, applied as a percentage of base rate (and many accessorial fees)

- Peak/demand surcharges — in 2025, both carriers' demand surcharges rose 6–9% over 2024 levels, with FedEx releasing surcharge details earlier each year

The DIM Weight Problem

Surcharges aren't the only invisible cost driver — dimensional weight pricing often delivers a bigger hit than shippers expect. Both UPS and FedEx use a standard DIM divisor of 139 for domestic shipments. The formula: (L × W × H) ÷ 139 = DIM weight. Carriers bill whichever is greater — actual weight or DIM weight.

For lightweight, bulky products, this means you may be paying for two or three times the actual weight of your shipment. Negotiating a higher DIM divisor — say, 166 or higher — directly reduces billable weight. At 50,000 shipments per year, even a modest per-package reduction compounds fast.

How to Conduct the Audit

Run through this process systematically:

- Pull 12 months of carrier invoices — every line item, not just the summary

- Map each surcharge to its contract definition — verify the rate applied matches what was agreed

- Calculate annual cost per surcharge category — multiply per-shipment fee by annual shipment count in that category

- Rank by dollar impact — focus negotiation energy on the top three to five fee categories first

- Flag billing errors — up to 5% of UPS and FedEx invoices contain billing errors, costing businesses thousands monthly in overcharges they never recover

That $6.50 residential surcharge? Across 50,000 shipments annually, it's $325,000 — before DAS or extended DAS fees stack on top. The math makes the audit non-negotiable.

Strategy 3: Negotiate Beyond Base Rates Using Market Benchmarks

The Most Common Negotiation Mistake

Focusing exclusively on base rates is the most costly mistake in parcel contract management. The carrier's published rate discounts are the opening position, not the end state. The real leverage is in the contract elements that most shippers never think to ask about.

Key negotiation targets beyond base rates:

- GRI caps — limit annual rate increases (often exclude accessorials unless specified)

- DIM divisor — negotiate above 139 to reduce billable weight for lightweight shipments

- Minimum charge reductions — FedEx offers fixed-dollar reductions; UPS uses percentages

- Surcharge discounts — residential, delivery area surcharge (DAS), and fuel surcharges are all negotiable — but carriers won't volunteer discounts here unless you ask specifically

Benchmark data is what gives these conversations teeth. Knowing what a carrier charges a comparable shipper — by volume, zone mix, and service type — tells you exactly where your contract is underperforming. Without that context, you're negotiating blind. Business Solutions Group's spend intelligence tools surface those comparisons so clients enter negotiations with specific targets, not general expectations.