Introduction

Employer-sponsored healthcare costs are accelerating at a pace that demands serious attention from business owners and HR leaders. According to Mercer's 2025 National Survey, total health benefit cost per employee rose 6.0% in 2025 and is projected to increase 6.7% in 2026 — the highest projected increase in 15 years.

For small employers, the picture is worse. Aon projected costs rising 10.3% before plan changes in 2025. Apply that rate over five years and benefits spend can double — crowding out payroll budgets and forcing an uncomfortable trade-off between competitive compensation and financial sustainability.

What many employers miss is that these increases aren't inevitable. They stem from specific, addressable decisions: how plans are structured, how benefits are monitored, and what workforce conditions surround the plan. The strategies below break down exactly where healthcare costs originate inside a business — and which levers have the most direct impact on controlling them.

Key Takeaways

- Healthcare cost growth compounds quickly — 6.7% annual increases mean per-employee costs double in roughly a decade

- Specialty and prescription drug spending now represents nearly 24% of total employer health spend

- Cost-shifting to employees is not a sustainable strategy — it harms retention without fixing root causes

- Claims data and benchmarking are prerequisites for targeted cost control

- Effective cost control requires continuous monitoring throughout the year — not just decisions made at annual renewal

How Healthcare Costs Build Up Inside a Business

Healthcare cost increases rarely arrive as a single, visible event. They accumulate steadily: annual premium renewals creeping up a few percent each cycle, specialty drug prescriptions renewing month after month, and claims frequency rising as more employees manage chronic conditions than a decade ago.

Much of this build-up stays hidden until renewal. Employers on fully insured plans often lack granular cost data throughout the year. By the time the next premium quote arrives, the damage is already done:

- Delayed preventive care has driven up downstream claims

- Ineligible dependents have remained enrolled undetected

- Pharmacy spend has accelerated without any intervention

The High-Cost Claim Problem

The escalation turns sharpest when triggered by a single high-cost event. One catastrophic hospitalization or a long-term specialty medication — a cancer therapy, an autoimmune biologic — can shift an entire plan's risk profile and push the following year's premium into a range the employer didn't plan for.

For smaller employers, where a handful of employees represent a significant share of the plan's risk pool, a single such claim can mean a 20–40% premium increase at next renewal. Waiting until that quote arrives to examine costs means there's little left to do except absorb the hit.

Key Cost Drivers Behind Rising Business Healthcare Expenses

Employer healthcare costs don't rise for a single reason — and the right intervention depends on which force is actually driving them. Two distinct pressures are at work:

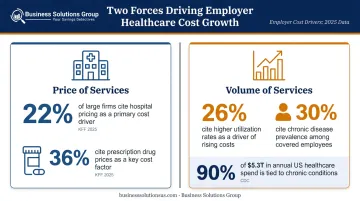

Price of services — set by provider consolidation, drug manufacturer pricing, and clinical labor market pressures. The 2025 KFF Employer Health Benefits Survey found 22% of large firms said higher hospital-service prices contributed "a great deal" to rising premiums, and 36% cited prescription drug prices.

Volume of services — driven by aging demographics, growing chronic disease prevalence, and increasing utilization. KFF found 26% of large firms identified higher utilization as a major premium contributor, and 30% cited chronic disease prevalence. The CDC reports that 90% of the nation's $5.3 trillion in annual healthcare expenditures go toward people with chronic and mental health conditions.

Prescription and Specialty Drug Spending

This is the fastest-growing and least-controlled cost driver for most employer plans. Business Group on Health reported that nearly 24% of employers' total healthcare spend in 2024 went to prescription drugs across medical and pharmacy benefits, with pharmacy benefit costs rising 7.7% in 2024.

GLP-1 medications for diabetes and weight management are a particular pressure point. Among firms with 5,000+ employees, 66% reported GLP-1 weight-loss coverage had a significant impact on prescription drug spending, according to KFF. Without formulary controls and real-time spend visibility, these costs compound year over year.

External pricing pressures are only part of the story. A significant share of cost growth comes from decisions made at plan design and procurement stages — and those are entirely within an employer's control.

Plan Design Decisions That Add Hidden Cost

- Plan structures that incentivize higher utilization

- Formularies without step therapy or prior authorization controls

- Dependent enrollment without eligibility verification

- Renewals signed without comparing current terms to market alternatives

Each of these represents a direct lever employers can pull — without waiting on market conditions to change.

Cost-Reduction Strategies for Business Healthcare

Effective cost reduction starts with identifying which dimension of the problem is most acute — plan design decisions, active management gaps, or surrounding workforce and market conditions. The right levers depend on your organization's size, risk profile, and claims history.

Strategies That Change Decisions

These approaches address choices made before or during plan design, procurement, and enrollment — where the longest-lasting financial impact is concentrated.

Evaluate funding model before each renewal. Switching from a fully insured plan to a high-deductible health plan (HDHP) paired with HSA contributions, or exploring level-funded arrangements, can reduce fixed premium exposure. Level-funded plans are already widely used — KFF found 37% of covered workers in firms with 10-199 employees were in level-funded plans in 2025. These arrangements offer more cost visibility than traditional fully insured plans and may return unused reserves at year-end if claims remain low.

Stop-loss insurance is a critical component; it caps the employer's exposure on any individual high-cost claim. Stability of workforce size matters — employers with volatile headcount should evaluate risk tolerance carefully before switching.

Build pharmacy benefit controls into plan design. Three controls matter most and all need to be in place at the design stage, not added reactively:

- Require less expensive drug options first through step therapy before approving costlier alternatives

- Tier formulary pricing based on cost and clinical equivalence to steer utilization

- Mandate prior authorization for high-cost prescriptions before they're filled

Without these controls, specialty drug spending escalates unchecked.

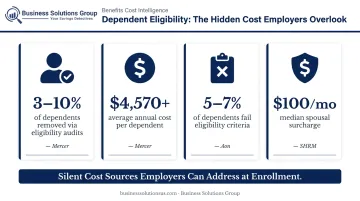

Enforce dependent eligibility and spousal coverage policies. Ineligible dependents remaining on employer plans is a well-documented source of silent cost escalation. Mercer estimates 3%–10% of dependents may be removed through eligibility audits, with an average annual incurred cost per dependent exceeding $4,570. Aon similarly finds 5%–7% of dependents typically fail eligibility criteria.

Dependent eligibility audits verify enrollment records against documentation requirements. Spousal surcharges — SHRM reports a median of $100/month — create a financial incentive for spouses with access to their own employer coverage to use it instead.

Benchmark plan specifications before signing. Employers who renew the same plan year after year without comparing market alternatives consistently overpay. Benchmarking examines whether current premium pricing, network discounts, and PBM contract terms actually reflect market rates. Business Solutions Group's spend intelligence and benchmark analysis capabilities — built around identifying cost inefficiencies across business operations — can be applied directly to healthcare benefit spend, giving organizations a clear picture of where their plan costs stand relative to peer benchmarks before signing the next renewal.

Strategies That Change How Benefits Are Managed

Most cost control failures happen during the plan year, not at purchase. These approaches improve visibility and oversight while the plan is active.

Use claims and utilization data to identify cost drivers. Reviewing claims data gives employers a targeted basis for adjustments — rather than across-the-board cuts that affect everyone indiscriminately. Key data categories to request from your insurer or TPA include:

- High-cost claimant distribution and claim type

- Chronic condition prevalence within the covered population

- Specialty drug utilization by therapeutic category

- Preventive care and primary care utilization rates

- Emergency department usage patterns

Reviewing this data quarterly — not just at renewal — allows course correction before costs compound.

Monitor PBM contract performance. PBM contracts contain negotiated discount terms that can underperform or deteriorate without scrutiny. Only about 60% of employers reported that their PBM passed through all rebates on traditional and specialty drugs, according to Drug Channels' 2023 analysis. The FTC has also flagged spread pricing and reimbursement practices among major PBMs that increase costs for employers.

Plan sponsors should verify regularly that contracted discounts are being applied correctly, that generic substitution rates are optimized, and that drug manufacturer rebates are flowing through as agreed.

Conduct regular benefits audits. Periodic audits of plan records — covering dependent eligibility, claims adjudication accuracy, and Medicare-eligible retirees — deliver some of the best returns available in benefits management, yet most employers skip them entirely. Removing even a handful of ineligible dependents at $4,570+ in annual cost each adds up quickly — and it requires only documentation review to execute.

Strategies That Change the Context Around Benefits

In many businesses, workforce demographics and market conditions drive costs just as much as plan design — sometimes more.

Build a preventive care culture. Businesses where employees regularly engage with preventive screenings, primary care, and chronic condition management programs generate fewer high-cost claims over time. That said, wellness programs are not a short-term cost solution — a JAMA randomized clinical trial found they improved some self-reported behaviors but did not significantly reduce medical spending during the study period.

The legitimate value is longer-term: reducing unmanaged risk factors like diabetes and hypertension that drive future claims frequency, and making mental health and EAP resources accessible before conditions escalate.

Access group purchasing power through pooled arrangements. Small and mid-sized employers purchasing coverage individually face pricing disadvantages that larger employers don't. NFIB found that 49% of small employers had taken a lower profit or suffered a loss to pay for health insurance premium increases over the previous five years. Group purchasing coalitions, professional employer organizations (PEOs), and multi-employer arrangements provide access to larger risk pools, better negotiated rates, and more competitive plan options than a small employer could secure independently. NAPEO reports a 27.2% annual ROI on PEO investment overall, though this reflects broad operational value rather than health-benefits-specific cost reductions.

Invest in year-round benefits education. Employees who don't understand how to use their benefits effectively tend to use more expensive care pathways unnecessarily. An employee who goes to urgent care or the ER for a condition that telehealth handles generates a claims cost that didn't need to happen. Consistent communication about network selection, telehealth options, and preventive benefit availability reduces this misutilization — and it doesn't require large budget investment to execute.

Conclusion

Controlling rising healthcare costs in business starts with accurate diagnosis. Whether the primary driver is plan design decisions made years ago, active management gaps that leave costs unmonitored throughout the year, or workforce and market conditions that create claims pressure the plan absorbs — the intervention differs by source. Defaulting to employee cost-shifting treats the symptom while the underlying causes continue to grow.

The businesses that consistently manage healthcare costs effectively share one characteristic: they treat it as an ongoing, data-driven process rather than an annual renewal decision. Continuous visibility into claims data, regular benchmarking, and proactive adjustments keep costs manageable without sacrificing the benefit quality that attracts and retains people.

Business Solutions Group's approach to healthcare cost management reflects this model. Their advisory relationships are built around continuous performance monitoring and spend intelligence — giving businesses the visibility to act on cost drivers before they escalate, not just at renewal time.

Frequently Asked Questions

How can businesses control rising healthcare costs?

Effective cost control means addressing multiple drivers at once: plan design, funding model, pharmacy spend, and workforce preventive care habits. Sustainable results require continuous monitoring and adjustment — not reactive changes made only at renewal.

What is the biggest driver of rising healthcare costs for employers?

While premium inflation reflects broad market forces, the largest controllable drivers are specialty and prescription drug spending, service volume from unmanaged chronic conditions, and plan design choices that allow ineligible dependents to remain enrolled or that lack pharmacy benefit controls.

Are self-insured or level-funded health plans a good option for small businesses?

Level-funded plans offer more cost visibility and the opportunity to recapture unused reserves at year-end, making them worth evaluating for businesses with reasonably stable workforce size. Stop-loss insurance is a critical component that protects against high individual claims. Assess your risk tolerance carefully before switching from a fully insured arrangement.

How does employee wellness actually reduce healthcare costs?

Wellness programs rarely reduce medical spending in the short term. The longer-term value lies in lowering high-risk factors — obesity, unmanaged diabetes, hypertension — that drive claims frequency and premium rates, while also reducing absenteeism from untreated chronic conditions.

What is value-based care and how does it help employers reduce healthcare costs?

Value-based care (VBC) ties provider payment to patient outcomes rather than service volume, prioritizing primary care over unnecessary hospitalizations. It can reduce overall utilization, but typically requires a defined network and clear employee communication to avoid adoption resistance.

How often should businesses review their employee health benefit plans?

Review plan performance data quarterly and conduct a full market comparison and benefits audit annually before renewal. Year-round monitoring of claims trends, pharmacy costs, and dependent eligibility outperforms waiting for a single annual review.