Introduction

Employer-sponsored health insurance costs are accelerating fast. According to Aon's 2025 analysis, the average cost per employee hit $12,893 in 2025 — up 7.2% from the prior year — with projections pointing to a 9.5% increase in 2026, potentially exceeding $17,000 per employee.

When premiums rise faster than revenue, the excess cost compresses operating margins, diverts capital from hiring and growth, and often forces reactive benefit cuts that erode employee morale.

The employers who feel this most acutely are the ones who treat renewals as an annual inconvenience rather than a managed cost category.

Healthcare costs don't become expensive by accident. Plan design choices, workforce health patterns, administrative processes, and vendor relationships all determine how much an employer ultimately pays. This article breaks down where costs actually originate and which strategies produce lasting savings without narrowing the coverage employees depend on.

This guide covers:

- Where employer healthcare costs actually originate

- Proven strategies that reduce spend without cutting benefits

- How plan design, vendor selection, and workforce health programs work together

Key Takeaways

- Chronic disease management and GLP-1 prescription spending are the fastest-growing cost drivers in employer plans right now

- HDHP/HSA pairing, dependent eligibility audits, and competitive carrier bidding cut costs through smarter plan structure

- Telehealth and pharmacy benefit optimization lower claims without narrowing employee access to care

- Preventive care and multi-year planning compound savings — reactive annual cuts rarely do

- Cost reduction doesn't require shifting financial burden onto employees — smarter plan design achieves both goals

How Healthcare Costs Build Up for Employers Over Time

Most employers underestimate their true healthcare spend because it doesn't appear as a single line item. The visible cost — premium contributions — is only part of the picture. The full burden includes:

- Direct plan costs: Employer premium share, claims reserves, stop-loss premiums

- Administrative overhead: TPA fees, compliance costs, open enrollment processing

- Indirect workforce costs: Absenteeism, reduced productivity, presenteeism from unmanaged health conditions

The Integrated Benefits Institute estimates that poor employee health costs U.S. employers $530 billion annually, including 1.4 billion lost workdays from absence and impaired performance. That figure captures what never shows up in a benefits renewal summary.

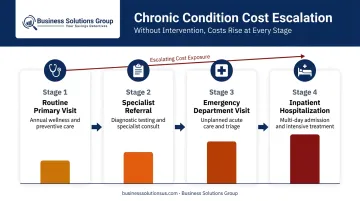

Why Costs Compound Over Time

Healthcare costs escalate because chronic conditions compound. An employee with an unmanaged condition progresses through increasingly expensive care settings — routine primary visits become specialist referrals, which become emergency department visits, which eventually become inpatient hospitalizations. Research on insured populations found that as the number of chronic conditions increases from 2 to 11, inpatient spending rises 22-fold.

Most employers only see this pattern clearly in hindsight, when annual claims data shows a spike in high-cost cases. By then, the cost has already been incurred. Employers who review utilization trends quarterly — rather than at renewal — catch these patterns early enough to intervene.

Quarterly visibility doesn't just flag problems sooner — it expands the range of interventions available before a manageable condition becomes a catastrophic claim.

Key Cost Drivers Behind Rising Healthcare Premiums

Understanding where costs originate lets employers target reductions precisely, rather than applying across-the-board cuts that erode coverage quality.

Chronic Disease and Workforce Demographics

The CDC reports that chronic and mental health conditions account for 90% of the nation's $5.3 trillion in annual healthcare expenditures. For employers, this translates directly to plan cost: a workforce with a higher prevalence of diabetes, hypertension, obesity, or behavioral health conditions will generate disproportionately high claims regardless of plan design.

Workforce age distribution matters too. Older employee populations and dependents drive more frequent specialist use, higher prescription volumes, and greater inpatient utilization — all of which push premium costs higher year over year.

Plan Design and Utilization Behavior

Employers often underestimate the relationship between plan structure and employee behavior. High copays and steep deductibles discourage employees from seeking early treatment, which appears to save money but frequently backfires. Deferred care for a manageable condition typically results in a higher-cost intervention later.

Conversely, poorly designed plans with low cost-sharing may generate unnecessary utilization of expensive settings — emergency rooms for conditions that urgent care could handle at a fraction of the cost.

Prescription Drug Costs

Pharmacy spend has become one of the fastest-growing cost categories in employer plans. WTW's 2025 analysis found pharmacy inflation increased 14% over 2024, outpacing medical inflation significantly.

GLP-1 medications for weight loss are a central factor. According to Evernorth's employer book-of-business data, weight-management medications accounted for 46.8% of the total increase in drug spending in 2024. Nearly 1 in 5 large employers now covers GLP-1s primarily for weight loss, per KFF's 2025 survey.

Administrative Inefficiency and Limited Visibility

Employers without regular claims reviews or vendor benchmarking processes systematically overpay without knowing where the excess originates. Administrative complexity, opaque PBM contracts, and infrequent competitive bidding all allow costs to build up undetected across consecutive plan years.

Cost-Containment Strategies for Healthcare Benefits

Effective strategies address one of three dimensions: how the plan is structured, how it's managed day-to-day, or the organizational environment that shapes healthcare demand. The goal across all three is to reduce spending without narrowing the scope of coverage employees can access.

Strategies That Reduce Costs by Changing Plan Design

These structural decisions set the cost baseline before the plan year begins.

Pair HDHPs with employer-funded HSA contributions. High-deductible health plans carry lower premiums than traditional PPO structures. When paired with employer contributions to a Health Savings Account, employees retain access to quality care through tax-advantaged savings while the employer reduces its annual premium base. For 2025, HSA contribution limits are $4,300 for self-only and $8,550 for family HDHP coverage.

Restructure plan tiers using actual utilization data. Demographic analysis — age distribution, family enrollment, specialist visit frequency — often reveals that employers are paying for coverage segments rarely used by their workforce. Designing tiers around real employee needs eliminates this structural overpayment.

Conduct dependent eligibility audits. Covered dependents who no longer qualify — adult children who have aged out, ex-spouses — silently inflate premium costs. According to a Mercer-cited study, approximately 11% of covered dependents were removed as ineligible during a dependent audit across 53 companies. That's a direct premium reduction with no impact on coverage quality for eligible employees.

Run competitive carrier bidding before each renewal. Accepting incumbent carrier increases without benchmarking alternatives is one of the most common and costly defaults in benefits management. A WTW 2025 survey found that 36% of employers have taken medical plans out to bid, with another 50% planning to do so — suggesting significant remaining opportunity for employers who haven't yet made bidding standard practice.

Strategies That Reduce Costs Through Active Benefits Management

These approaches reduce the number and severity of claims while the plan is active.

Expand telehealth and actively promote use. Virtual care visits cost notably less per encounter than in-person visits. A 2023 AJMC study of a large academic health system's employee population found a mean per-episode cost of $379.76 for telemedicine versus $493.49 for non-telemedicine encounters — a difference of roughly $114. Telehealth is particularly effective for routine primary care, mental health check-ins, and chronic condition management.

Promotion matters as much as availability. Employers who add telehealth without actively communicating when and how to use it see minimal adoption — and minimal savings.

Invest in employee health literacy. Employees who know when to use urgent care instead of the ER, how to request generics, and how to flag billing errors make lower-cost decisions at every step. Education delivered through open enrollment seminars, digital tools, and on-demand resources creates behavior change that compounds over time.

Apply claims data and spend analysis to identify utilization patterns. Reviewing aggregate claims data surfaces which conditions, procedures, or employee cohorts are driving disproportionate spend. Business Solutions Group applies this same spend intelligence discipline to supply chain and operational cost categories — and it translates directly to healthcare. A cluster of high-cost musculoskeletal claims, for instance, points toward targeted physical therapy or telemedicine interventions rather than broad cost-shifting.

Optimize pharmacy benefits. Generic substitution, prior authorization for specialty drugs, and step therapy protocols all reduce pharmacy spend without limiting employee access to necessary medications. The FTC cites FDA estimates that generic drugs typically cost 80–85% less than their brand-name equivalents — making formulary management one of the highest-leverage pharmacy cost controls available.

Strategies That Reduce Costs by Reshaping the Organizational Context

These longer-horizon strategies often produce the highest return on investment, though results take multiple plan years to materialize.

Build preventive care and wellness programs. RAND research found that disease management components of workplace wellness programs generated an estimated ROI of $3.80 for every $1 invested — significantly higher than the roughly $0.50 return from lifestyle programming alone. High-impact program components include:

- Biometric screenings and chronic disease management

- Weight management support and smoking cessation

- Condition monitoring before low-cost issues escalate into high-cost claims

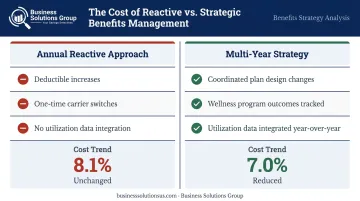

Adopt a multi-year healthcare cost strategy. Annual premium negotiations without a longer-term plan produce incremental savings at best. WTW data shows that employers using coordinated plan changes reduced projected 2025 cost trend from 8.1% to 7.0% — but these reductions are more durable when plan design changes, wellness program outcomes, and utilization data are integrated across multiple years rather than treated as independent annual decisions.

Support flexible work and employee well-being. Chronic workplace stress is a documented driver of increased healthcare consumption. Research published in the American Journal of Preventive Medicine estimates that employee disengagement and burnout cost employers approximately $4,000–$4,300 per nonmanagerial employee annually. Flexible scheduling, remote work options, and robust Employee Assistance Programs reduce stress-related claims and absenteeism — creating healthcare cost relief that doesn't appear in plan design at all.

Partner with knowledgeable brokers for ancillary benefit bundling. Brokers with established carrier relationships access rates and plan structures unavailable to individual employers. Bundling medical, dental, vision, and disability coverage through a single advisory relationship often unlocks pricing tiers typically available only to larger organizations — a practical way for mid-size employers to gain purchasing leverage they couldn't achieve independently.

Conclusion

Healthcare costs are not an uncontrollable external force. They are shaped by plan design decisions, benefit management practices, and the organizational conditions employers create. Every employer that has accepted consecutive years of premium increases without auditing its dependents, reviewing its claims data, or benchmarking its carriers has paid more than necessary — and reduced coverage unnecessarily in the process.

Employers who treat healthcare benefits as a managed cost center apply the same discipline to spend analysis, vendor benchmarking, and utilization monitoring that they bring to procurement and logistics. That approach consistently produces better financial outcomes without stripping the coverage that keeps employees healthy and productive.

The starting point is knowing where costs actually originate — then building a strategy around that data rather than around annual renewal pressure.

Frequently Asked Questions

What are the five key needs that contribute to healthcare cost-minimizing strategies?

The five core needs are plan design optimization, preventive care access, employee education, data-driven utilization management, and strategic multi-year planning. Used together, they consistently outperform any single tactic.

How do you improve employee satisfaction with healthcare benefits?

Satisfaction improves when employees have genuine access to quality care, understand how their benefits work, and face manageable out-of-pocket costs. Cost-cutting that shifts financial burden onto employees tends to reduce satisfaction even when headline premiums appear lower.

Can employers reduce healthcare costs without increasing employee out-of-pocket expenses?

Yes. Dependent eligibility audits, telehealth promotion, pharmacy optimization, and preventive care investment all reduce employer spend without shifting costs to employees. Some plan redesigns involve tradeoffs, but many effective strategies are cost-neutral or beneficial for employees.

What role does preventive care play in controlling employer healthcare costs?

Preventive care reduces the frequency and severity of high-cost claims by catching conditions early and managing chronic disease risk factors before they escalate. That benefit compounds over time as fewer employees reach the costly intervention stages of untreated chronic conditions.

How does a multi-year healthcare strategy differ from annual cost-cutting?

Annual cost-cutting typically involves reactive changes (raising deductibles, switching carriers) without addressing the underlying drivers. A multi-year strategy integrates wellness outcomes, utilization trend data, and plan design refinements to systematically reduce the conditions that generate high-cost claims year over year.

What is the 3 C's framework in employer healthcare benefits?

Cost, Coverage, and Care quality represent the three dimensions employers must balance in benefits strategy. The goal is to optimize all three simultaneously, rather than trading coverage quality or employee costs for short-term budget relief.