Introduction

Family premiums for employer-sponsored health coverage now average $26,993 per year, according to the KFF 2025 Employer Health Benefits Survey—and that figure rose 6% from the prior year alone. For small and mid-sized businesses, this isn't just a benefits line item. It compresses payroll budgets, limits hiring capacity, and squeezes margins at exactly the moment when competing for talent requires staying competitive on total compensation.

What those numbers don't show is how much of that cost is controllable. A meaningful portion flows directly from plan design decisions made years ago, unmanaged chronic conditions, and renewal cycles where the default answer was "renew as-is."

What follows covers how employer healthcare costs actually accumulate, what's driving them today, and specific strategies—organized by where they intervene—that produce real savings without stripping employees of meaningful coverage.

Key Takeaways

- Average family premiums now exceed $26,993/year, with employers covering roughly 74% of that cost

- Costs compound gradually through passive renewals, untreated chronic conditions, and rising pharmacy spend

- The biggest controllable drivers: plan design structure, workforce health risk, and prescription drug spend

- Effective strategies target plan design, active health management, and pharmacy spend—not benefit cuts

- Optimizing plans using claims data protects both your budget and employee satisfaction

How Employer Healthcare Costs Typically Build Up

Most employers don't experience a sudden cost explosion. The buildup is gradual, which makes it easy to miss until the damage is already done.

Annual premium renewals consistently outpace general inflation. A workforce with unmanaged chronic conditions generates steadily higher claims each year, which drives higher renewal premiums the following year. That cycle compounds quietly until it shows up as a 7–8% renewal increase that feels unavoidable.

Several cost patterns stay invisible until someone actually looks for them:

- Specialty drug spend that isn't tracked separately from general pharmacy costs

- Emergency room visits for conditions that could have been handled through urgent care or telehealth

- Underutilized benefits renewed automatically year after year without review

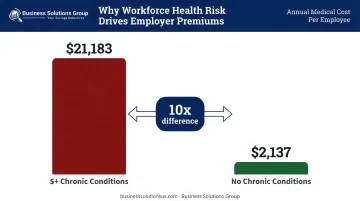

Those invisible patterns hit harder when chronic disease is factored in. Research published in AJMC found that working-age adults with five or more chronic conditions averaged $21,183 in annual medical costs, versus $2,137 for those with none. That tenfold difference doesn't disappear at renewal — it folds directly into the following year's premium calculation.

Breaking that cycle requires knowing where the money is actually going — and that starts with the right cost management strategies.

Key Cost Drivers for Employer Healthcare Spend

Understanding where costs originate is the prerequisite to controlling them. Four drivers dominate.

Plan Design Structure

The structure of deductibles, copays, coverage breadth, and prescription drug tiers determines both the premium employers pay and the claim volume that flows through the plan. Initial plan selection is one of the highest-leverage decisions an employer makes—yet many employers renew without revisiting whether the design still fits their workforce.

Workforce Health Risk Profile

According to the CDC, 90% of U.S. annual healthcare expenditures are for people with chronic and mental health conditions. With obesity affecting over 40% of U.S. adults and hypertension rates reaching 52.5% among those aged 40–59, most employer populations carry substantial chronic disease risk. Employees who don't engage with preventive care generate more claims—and more expensive ones—over time.

Prescription and Specialty Drug Spend

Pharmacy costs are accelerating faster than other plan components. Mercer's 2024 employer survey found pharmacy benefit costs rose 7.7% in 2024, following an 8.4% increase in 2023. The employer median for pharmacy's share of total healthcare dollars climbed from 21% in 2021 to 24% in 2024. Specialty drugs and biologics are the primary driver, and few employers have built systems to control this cost before it compounds.

How Context Shapes Your Cost Profile

No two employers face identical cost profiles. The dominant driver shifts based on:

- Employer size (self-funded vs. fully-insured dynamics)

- Geographic market and local provider pricing

- Workforce age and demographic mix

- Current plan design and deductible structure

Knowing which driver is actually pushing your costs up is what makes the difference between a fix that works and one that doesn't.

Cost-Reduction Strategies for Employer Healthcare Costs

No single strategy works universally. The most effective approach depends on first diagnosing where costs originate, then selecting strategies that address the right lever. The three levers map to: decisions made around plan design, how the plan is actively managed once live, and the broader structural context in which it operates.

Strategies That Reduce Costs by Changing Decisions

These are the choices made before or around how the health plan is structured and administered. They set the cost ceiling for everything that follows.

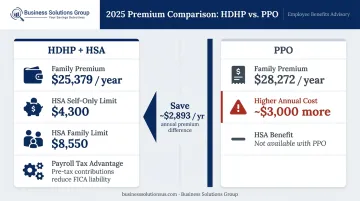

Shift to an HDHP paired with an HSA

High-deductible health plans carry lower premiums than traditional options. KFF's 2025 data shows the gap is substantial:

- HDHP/savings option (family coverage): $25,379/year

- PPO (family coverage): $28,272/year — nearly $3,000 more per family

Currently, 36% of firms offer an HDHP with a savings option, and 33% of covered workers are enrolled in one.

The key implementation requirement: pair the HDHP with employer-seeded HSA contributions so employees can absorb higher deductibles without financial hardship. For 2025, HSA contribution limits are $4,300 for self-only coverage and $8,550 for family coverage. Employer HSA contributions are excluded from employees' gross income and carry payroll tax advantages for the employer as well.

Evaluate self-funded vs. fully-insured plan models

67% of covered workers are in self-funded plans nationally, but only 27% of workers at small firms (10–199 employees) are—compared to 80% at large firms. Self-funded arrangements give employers direct access to claims data, more flexibility in plan design, and the ability to select vendors independently rather than accepting a carrier's bundled offering.

Financial risk exposure is the main downside. Stop-loss insurance is the standard mitigation, capping catastrophic claims at a defined threshold. For mid-sized employers, level-funded plans offer a middle path:

- Fixed monthly payments provide cost predictability

- Potential year-end refunds if claims run below projections

- Lower barrier to entry than fully self-funded arrangements

Right-size plan design elements and audit benefits utilization

Adjusting cost-sharing structures—raising copays for brand-name drugs, tiering specialist visits, restructuring prescription drug formularies—can reduce premiums while preserving access to care. The critical requirement: model changes against actual claims data rather than applying uniform adjustments that may penalize employees who rely on specific treatments.

Before each renewal, audit which benefits employees actually use. Removing or restructuring low-utilization benefits and redirecting that budget toward high-value offerings produces savings without reducing the overall quality of the package.

Strategies That Reduce Costs by Changing How Benefits Are Managed

These are ongoing levers. Their value compounds over time as employee behavior and health outcomes improve.

Invest in employee health literacy and benefits education

Employees who don't understand their plan default to expensive choices. Common patterns include:

- Using emergency rooms for non-emergency conditions

- Avoiding generic drugs in favor of costlier brand-name alternatives

- Skipping preventive screenings that could catch high-cost conditions early

Annual open enrollment guides, decision-support tools, and periodic education sessions redirect these behaviors—reducing claim volume across the entire plan.

Deploy telehealth with appropriate utilization incentives

RAND research found that for acute respiratory infections, telehealth service costs were roughly 50% lower than physician office or emergency department visits. The utilization caveat matters: RAND also found direct-to-consumer telehealth sometimes increased net annual spending by roughly $45 per user when visits represented new utilization rather than substituting for existing care.

Telehealth works best as a substitution tool for conditions employees would otherwise bring to urgent care or the ER—not as an add-on service for conditions they'd otherwise manage at home.

Launch wellness programs targeting high-risk employees

RAND's analysis of workplace wellness programs found an overall ROI of approximately $1.50 saved per dollar invested, with disease management components producing materially larger savings than lifestyle management alone. A 2019 JAMA randomized trial found improvements in self-reported behaviors but no significant short-term effect on healthcare spending—a useful caution against overstating near-term financial returns.

Wellness programs are a risk-management investment. Well-designed programs reduce the share of employees in high-risk cost categories over time, which reduces claim frequency and severity—and eventually, renewal premiums. Short-term ROI varies; long-term population health impact is more consistent.

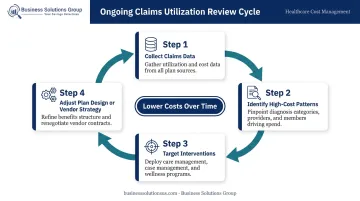

Conduct regular claims utilization reviews

Reviewing claims data quarterly or annually identifies high-frequency diagnoses, overused services, and gaps in preventive care uptake. This creates the foundation for targeted interventions—adjusting plan design, redirecting vendor relationships, or launching specific wellness initiatives aimed at the conditions actually driving cost in the current workforce.

Strategies That Reduce Costs by Changing the Context Around Benefits

These strategies address external factors: network structure, carrier relationships, tax programs, and how healthcare fits into broader cost management.

Reconfigure provider networks using tiered or narrow designs

Tiered networks incentivize employees to use lower-cost, higher-quality providers by reducing cost-sharing at preferred tiers. Narrow networks limit the plan to a defined set of cost-effective providers, producing lower premiums in exchange for reduced provider choice. Large employers can pursue direct contracting with health systems for high-cost service categories—particularly elective surgeries and specialty care—bypassing standard commercial rates entirely.

Employee acceptance is a real constraint. Tiered networks generally produce less resistance than pure narrow networks, making them the more practical starting point for most mid-sized employers.

Negotiate directly with carriers and access group purchasing power

Many employers accept renewal terms without presenting claims data or benchmarking their plan against comparable groups. Arriving at renewal negotiations with actual utilization data, benchmark comparisons, and bundled medical/dental/vision purchasing consistently produces better outcomes than passive acceptance.

Smaller employers without individual purchasing power can access better pricing through Association Health Plans or professional employer organizations that pool purchasing across multiple groups. Savings outcomes vary, so verify any claims against current market benchmarks before committing.

Use applicable tax programs and regulatory options

Small businesses with fewer than 25 full-time equivalent employees, average wages below the inflation-adjusted threshold, and employer premium contributions of at least 50% may qualify for the ACA small business healthcare tax credit of up to 50% of premium costs through SHOP marketplace participation. Health Reimbursement Arrangements (HRAs) offer additional flexibility for employers seeking tax-advantaged ways to fund employee coverage outside traditional group plan structures.

Apply spend intelligence to treat healthcare as a managed cost center

Healthcare is the second or third largest expense line item for most businesses. Few employers subject it to the same analytical rigor as other major cost categories. Benchmarking premiums against comparable groups, reviewing claims data systematically, and entering renewal negotiations with hard data consistently produces better outcomes than passive acceptance.

Business Solutions Group's healthcare cost reduction program applies this analytical discipline to employer health spend. Working with businesses of 25 or more employees, their approach includes a no-cost savings analysis, detailed benchmarking against wholesale pricing benchmarks, and a structured implementation process that typically produces $100–$300+ in savings per employee per month without disrupting existing coverage or transferring costs to employees.

Conclusion

Managing employer healthcare costs isn't about reducing benefits—it's about understanding where costs actually originate and intervening at the right lever. Plan design decisions set the cost ceiling. Active management determines whether claims escalate or stabilize over time. Structural context—networks, carrier relationships, tax programs, and benchmarking discipline—determines whether you're paying market rates or retail rates for the same coverage.

Employers who consistently control costs treat healthcare as a managed cost center. They review utilization data on a regular cadence, benchmark against relevant peers, and negotiate from a position of information rather than inertia. That discipline is what keeps savings durable past the first renewal cycle—not just achievable in it.

Frequently Asked Questions

What percentage of healthcare costs are paid by employers?

According to KFF's 2025 data, employers cover 84% of single coverage premiums and 74% of family coverage premiums on average. Workers contribute the remainder—$1,440 for single coverage and $6,850 for family coverage annually. These shares vary based on employer size, industry, and plan type.

What is the 80/20 rule in healthcare?

The 80/20 principle in healthcare refers to the concentration of spending among a small portion of the population. National data shows the top 5% of people account for roughly half of all health spending, averaging over $72,000 annually—targeting this group with disease management programs typically delivers the highest ROI on cost-containment efforts.

How much does it cost to hire an employer healthcare cost consultant?

Fees vary widely—from commission-based brokers paid by carriers to fee-only advisors charging flat or hourly rates. Firms like Business Solutions Group offer a no-cost initial savings analysis before any engagement begins, with advisory costs typically recovered many times over through improved plan design and reduced premiums.

What is the difference between a self-funded and fully-insured health plan?

Fully-insured plans involve paying a fixed premium to a carrier that assumes all claims risk. Self-funded plans have the employer pay claims directly—often with stop-loss insurance capping catastrophic exposure—giving larger employers more plan design flexibility, direct claims data access, and potential savings. The trade-off is greater financial responsibility.

How can small businesses reduce healthcare costs without cutting employee benefits?

Several approaches lower costs without reducing coverage:

- HDHP + HSA combinations — lower premiums while preserving comprehensive coverage

- SHOP marketplace — qualifies small businesses for the ACA small business tax credit

- Health Reimbursement Arrangements — employer-funded, tax-efficient benefit accounts

- Telehealth adoption — reduces per-visit costs for routine and urgent care

- Wellness programs — address chronic disease risk before it drives claims

What is an HSA and how does it help reduce employer healthcare costs?

An HSA is a tax-advantaged account paired with an HDHP, allowing employees to save pre-tax dollars for qualified medical expenses—reducing the financial burden from higher deductibles. Employers benefit from lower HDHP premiums, and any employer HSA contributions are excluded from gross income—reducing payroll tax liability on both sides.