Introduction

Family premiums for employer-sponsored health coverage now average $25,572 per year, according to the KFF 2024 Employer Health Benefits Survey — a figure that is 52% higher than it was in 2014. Single coverage averages an additional $8,951 annually, with costs rising 6–7% in just the past year.

For most employers, that math compounds fast. A workforce of 200 employees facing a 7% annual premium increase adds hundreds of thousands of dollars to the benefits budget, before a single new hire or benefit enhancement is considered.

Health insurance now represents 6.9% of total private-sector compensation, per the Bureau of Labor Statistics, making it one of the largest controllable labor cost lines on the books.

These costs are not fixed. They rise when employers make suboptimal decisions at renewal, when employees lack the information to navigate care efficiently, and when the structural setup around a plan goes unexamined. What follows breaks down all three dimensions: what drives healthcare costs up and what actually brings them down.

Key Takeaways

- Family premiums have risen 52% over the past decade, with specialty drug costs pushing premiums even higher

- The biggest cost drivers are chronic condition claims, specialty drug spend, poor plan design, and gaps in employee health literacy

- Effective strategies span plan design changes, utilization management, and structural moves like self-funding or pooled purchasing

- The goal is eliminating waste and reducing claims root causes — not just shifting costs to employees

How Employer Healthcare Costs Build Up

Healthcare spending doesn't arrive as a single invoice. It accumulates through several parallel channels that individually seem manageable but create real pressure when combined.

The Gradual and the Episodic

Cost build-up happens in two patterns:

- Gradual (premium creep): Annual renewal increases of 5–10% compound quietly. An employer who accepted a 7% increase every year for five years is now paying 40% more than they were — often without realizing the trajectory

- Episodic (claims spikes): A cluster of high-cost claims in a single plan year — cardiac events, premature births, complex surgeries — can trigger a sharp renewal increase that gets embedded into the base rate going forward

By the time the renewal letter arrives, the damage is already priced in — and the window to push back has closed.

Hidden Cost Layers

Beyond premium trends and claims spikes, a second category of costs hides in plain sight. These don't appear in the renewal letter — they require someone to actually dig into the plan data:

- Benefits that are funded but rarely used

- Ineligible dependents enrolled on the plan

- Employees using emergency rooms for conditions treatable at urgent care

- Prescription spend inflated by the absence of formulary controls

- Administrative fees buried in carrier arrangements that were never benchmarked

Every item on this list is fixable — but only once it's been identified. That requires a deliberate audit, not a passive review of the annual renewal.

Key Cost Drivers for Employer Healthcare

Workforce Health Risk

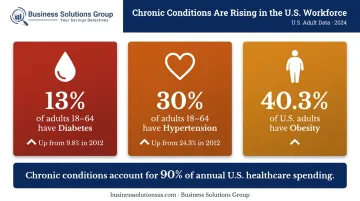

The chronic disease burden in the American workforce is substantial. CDC data from 2024 shows that 13% of adults aged 18–64 have diagnosed diabetes (up from 9.8% in 2012) and 30% have diagnosed hypertension (up from 24.3% in 2012). Adult obesity affects 40.3% of U.S. adults, with rates highest among those aged 40–59.

These conditions don't just generate baseline claims — they escalate. Undermanaged diabetes leads to hospitalizations. Uncontrolled hypertension leads to cardiac events.

Chronic conditions and mental health account for 90% of annual U.S. healthcare spending, per CDC estimates. Employers with higher-risk workforce populations absorb that disproportionately in their claims.

Plan Design Choices

Plans with low deductibles and broad, unrestricted networks remove the financial friction that guides employees toward cost-effective care. The result: overutilization of services that could have been handled at lower cost.

Common examples:

- ER visits for non-urgent conditions

- Brand-name prescriptions when generics exist

- Out-of-network specialist visits when in-network alternatives are available

These aren't bad employee decisions — they're predictable responses to a plan design that offers no reason to choose differently.

Prescription Drug Spend

Pharmacy is now one of the fastest-moving cost lines in employer health plans. Per CVS Caremark's 2023 Drug Trend Report, the numbers tell a stark story:

- Specialty drugs represent 53% of total drug spend — used by fewer than 2% of patients

- The overall commercial drug trend ran 7.9% in 2023

- GLP-1 coverage is now offered by 44% of large employers and 64% of employers with 20,000+ employees

GLP-1 medications for obesity are accelerating this further. Mercer's 2024 survey found pharmacy benefit costs rose 7.7% in 2024. Employers without formulary controls are absorbing this growth with no mechanism to slow it.

Employee Health Literacy

When employees don't understand their plan, they make expensive decisions by default. Not knowing that urgent care is appropriate (and far cheaper) for most non-emergency situations — or that a 90-day generic mail order costs less than three brand-name copays — means the plan pays more than it needs to, every time.

Low health literacy compounds every other cost driver. Better-informed employees make better choices — and that difference shows up in claims data.

Cost-Reduction Strategies for Employer Healthcare

Effective strategies work on three layers: how the plan is designed before it launches, how it's used while it's active, and what structural conditions surround it.

Strategies That Change Plan Design Decisions

Switch to Consumer-Directed Health Plans (HDHPs with HSAs)

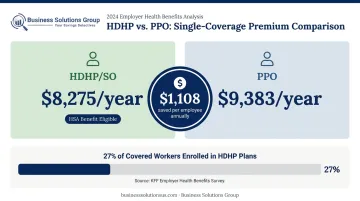

HDHP premiums are measurably lower than traditional plans. KFF 2024 data shows HDHP/SO single premiums at $8,275 vs. $9,383 for PPOs — a difference of over $1,100 per employee annually. Pairing HDHPs with Health Savings Accounts gives employees a tax-advantaged way to cover higher out-of-pocket costs, softening the financial shift.

Currently, 27% of covered workers are enrolled in HDHP/SO plans. The model works, but only when employees understand how HSAs function. Without education, HDHPs can create financial hardship rather than shared savings.

Benchmark Carriers Before Every Renewal

Most employers accept renewal increases without running a comparative analysis. Conducting a benchmarking exercise before each renewal — comparing premiums, network quality, administrative fees, and claims performance across carriers — creates negotiating leverage and often surfaces materially better options.

Business Solutions Group's healthcare advisory services include a complimentary benchmark analysis that examines current contract and pricing structures. Their research consistently finds that **96% of U.S. employers are still paying retail prices for employee healthcare**, and that wholesale-priced alternatives generally run 30–70% less than pre-packaged plans.

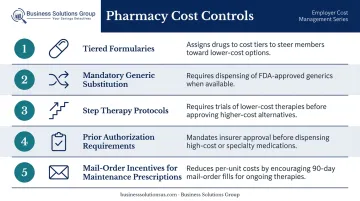

Restructure Prescription Drug Benefits

Employers can reduce pharmacy spend by implementing:

- Tiered formularies that favor generics and preferred drugs

- Mandatory generic substitution where therapeutically equivalent

- Step therapy protocols before approving specialty drugs

- Prior authorization requirements for high-cost medications

- Mail-order incentives for maintenance prescriptions

These controls reduce spend without eliminating access to necessary medications.

Working Spouse Provisions and Opt-Out Incentives

Offering cash incentives for employees who opt out when covered under a spouse's plan, or requiring working spouses to exhaust their own employer's coverage first, reduces dependent enrollment costs. These arrangements require careful structuring under HIPAA and applicable state regulations, but they're well-established and legally sound when implemented correctly.

Strategies That Change How Healthcare Is Managed

Deploy Wellness Programs Targeting Chronic Conditions

Wellness initiatives show the most financial impact when focused on conditions that generate the most claims: diabetes management, smoking cessation, hypertension screening, and obesity programs.

Participation is the key variable. RAND research found that HRA completion rates were 63% with incentives vs. 29% without. Programs with low participation have limited financial effect — which is why incentive design and multi-channel communication aren't optional components.

Make Telehealth the Default First Point of Care

Telehealth visits cost a fraction of in-person and emergency room visits for the same presenting conditions. According to FAIR Health's 2025 analysis, telehealth represented 3.8% of all medical claim lines in 2023 — still well below its potential as a first point of care.

The gap between adoption and potential is largely behavioral. Employers who actively communicate telehealth access (not just include it in open enrollment materials) and remove barriers to use — like copays or confusing enrollment steps — see meaningfully higher utilization and lower overall claims.

Use Claims Data to Find and Act on Cost Outliers

Aggregate health plan data contains patterns worth acting on that most employers never fully analyze. Claims patterns, high-utilization services, ER usage rates, and prescription spend by category all point to intervention opportunities — if someone is looking at them with the right framework.

Business Solutions Group applies this kind of forensic analysis as part of its healthcare engagements. Their team examines current healthcare structures, identifies where costs are actually originating, and assembles targeted strategies based on what the data reveals. Reviewing claims data doesn't require exposing individual employee information — properly structured analysis operates at the aggregate level, fully within HIPAA parameters.

Educate Employees Year-Round

Open enrollment is not enough. Employees who receive benefits education only once a year forget how to use their plan within weeks. Regular communication — explaining when urgent care is appropriate, how to use an HSA, how to compare in-network provider costs — directly affects utilization patterns.

Business Solutions Group's program includes employee onboarding and ongoing education as a core service component, not an afterthought. Maximizing program adoption is what converts plan design improvements into actual claims reductions.

Strategies That Change the Context Around Healthcare

Evaluate Self-Funded Plans

In a self-funded arrangement, the employer pays claims directly rather than paying premiums to an insurer. This eliminates insurer profit margins, provides greater plan design flexibility, and offers cash-flow advantages since funds aren't pre-paid.

KFF 2024 data shows 63% of covered workers are already in self-funded plans — 79% at large firms, but only 20% at small firms. The model is most viable for employers with approximately 100+ employees and stable claims histories. Stop-loss insurance, carried by 75% of covered workers in large self-funded plans, caps catastrophic exposure and makes the risk profile manageable.

Pool Purchasing Power

Smaller employers who lack individual negotiating leverage can access better carrier rates and plan terms through:

- Purchasing cooperatives

- Professional Employer Organizations (PEOs)

- Multi-employer group arrangements

NAPEO research indicates businesses using PEOs can achieve meaningful cost savings, alongside lower employee turnover and stronger benefit access than comparable non-PEO companies. For companies below the threshold for self-funding, pooled purchasing is often the most practical route to better plan economics.

Address Workplace Conditions Driving Utilization

Employee burnout, chronic stress, and inadequate mental health support generate healthcare utilization that no amount of plan restructuring will reduce. The plan isn't causing the problem.

A 2025 meta-analysis published in the Journal of Health Economics and Outcomes Research, covering 19 employer-specific studies and over 42,000 participants, found a pooled ROI of 2.3x for enhanced behavioral health programs, with annual net savings averaging 14.3%. Employers who invest in flexible work arrangements, mental health benefits, and Employee Assistance Programs address upstream causes of claims, not just the downstream costs.

Conclusion

Employers who consistently manage healthcare costs share a common approach: they don't wait for renewal season to act. They analyze claims data year-round, educate employees continuously, revisit plan design with purpose, and re-examine the structural setup around their benefits regularly.

Defaulting to benefit cuts or cost-shifting to employees is the path of least resistance. It erodes coverage quality, creates retention risk, and leaves the underlying drivers of spend untouched. The strategies covered in this article take a different approach — targeting where costs actually originate:

- Restructuring HDHPs with HSA support to reduce premiums without gutting coverage

- Auditing claims and pharmacy spend to catch waste and billing errors

- Investing in behavioral health and preventive care to reduce downstream utilization

- Evaluating self-funded or level-funded arrangements for employers with sufficient scale

- Using carrier and vendor data to negotiate from an informed position at renewal

None of these require a massive benefits overhaul. Most start with better data and a willingness to question default assumptions.

Frequently Asked Questions

Frequently Asked Questions

How can employers reduce healthcare costs?

The most effective approach combines smarter plan design (HDHPs, carrier benchmarking), utilization management (telehealth, wellness programs), and structural changes like self-funding or pooled purchasing. The right mix depends on workforce size, risk profile, and current plan performance.

What is a high-deductible health plan (HDHP) and how does it lower employer costs?

HDHPs reduce employer premium costs by shifting a larger share of initial medical expenses to employees. They work best when paired with HSAs, which give employees a tax-advantaged way to cover those costs. Without clear employee education, though, the model creates financial hardship rather than the shared savings it's designed to deliver.

Do workplace wellness programs actually reduce healthcare costs?

Wellness programs deliver the most measurable impact when they target high-claims conditions like chronic disease management and smoking cessation. RAND research shows incentives nearly double participation rates, making communication and incentive design the primary factors in whether the investment pays off.

What is self-funded health insurance and when does it make sense?

In a self-funded plan, the employer pays claims directly rather than pre-paying premiums — with stop-loss insurance capping catastrophic risk. The model works best for employers with 100+ employees and stable claims histories, eliminating insurer profit margins while enabling direct plan design control.

How can small businesses reduce healthcare costs without cutting coverage?

Small businesses can reduce costs by joining purchasing cooperatives or PEOs for group buying power, offering HDHPs with HSAs, benchmarking carriers before renewal, and promoting telehealth and wellness programs that reduce claims frequency — preserving meaningful coverage while controlling what they spend on it.

How does telehealth help lower employer healthcare expenses?

Telehealth visits cost significantly less than in-person or emergency room care for the same conditions. Employers who make telehealth the default first point of care — through active communication and low-barrier access — see lower overall claims costs compared to those who treat it as a rarely-used benefit add-on.