Introduction

Employer-sponsored health insurance now costs an average of $25,572 per year for family coverage and $8,951 for single coverage, according to the KFF 2024 Employer Health Benefits Survey. Employers cover roughly 75–84% of those premiums — meaning family coverage alone costs businesses over $19,000 per employee annually.

Run that math across 50 employees, and you're looking at nearly $1 million in healthcare spend before a single other operating expense.

The trajectory makes this harder to absorb. KFF reports premiums rose 6–7% in 2024, and Mercer projects the highest cost increase in 15 years for 2026. For small and mid-sized businesses where healthcare is often the second or third largest line item on the P&L, that compounding trend steadily erodes margin year after year.

The good news: much of what employers pay is shaped by decisions they control. Plan design choices, day-to-day plan management, and how coverage is purchased all drive costs — and all can be optimized. This article covers the most effective levers across each of those areas.

Key Takeaways

- Employer-sponsored premiums rose 6–7% in 2024 and are projected to climb further through 2026

- Most overspending builds through inertia — auto-renewals and unreviewed plan structures go unchallenged year after year

- Key cost drivers: plan design, workforce demographics, pharmacy spend, claims patterns, and carrier pricing

- Effective reduction works across three dimensions: plan design decisions, day-to-day plan management, and purchasing context

- No single fix works alone — layered strategies deliver sustainable savings without reducing employee benefits

How Group Health Insurance Costs Build Up

Premium increases rarely feel catastrophic in any single year. A 6% increase seems manageable. But that's compounding on an already-elevated base — and over time, the effect is substantial.

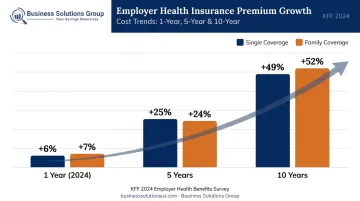

KFF's long-term data tells the story clearly:

| Timeframe | Single Coverage Increase | Family Coverage Increase |

|---|---|---|

| 1 year (2024) | 6% | 7% |

| 5 years | 25% | 24% |

| 10 years | 49% | 52% |

Source: KFF 2024 Employer Health Benefits Survey

For an employer that absorbed those increases passively — without renegotiating plan design or shopping carriers — family premiums that cost $17,000 a decade ago now cost over $25,000. Per employee. Every year.

Why Inertia Is Expensive

Inertia is the core problem, not the market itself. Most employers encounter their healthcare costs as a lump-sum renewal number, with limited visibility into what drove the increase — whether it was claims growth, demographic shifts, carrier pricing adjustments, or plan design inefficiency.

SHRM recommends employers put benefits contracts out to bid at least every three to five years to test competitive pricing. Many go far longer without a structured review.

The result: costs that look stable year-over-year but are compounding into a significantly larger liability by the time the next renewal forces the issue.

Key Cost Drivers for Group Health Insurance

Not all cost drivers are within an employer's control, but knowing which ones are is the first step toward a real reduction strategy.

Workforce and Plan Design Factors

- Workforce demographics — older workforces and those with higher rates of chronic conditions generate more claims and push premiums higher

- Geographic location — state regulations and local market concentration affect carrier pricing significantly

- Plan comprehensiveness — low-deductible, rich-benefit plans carry higher premiums; the actuarial value of the plan directly affects what employers pay

- Claims history — in large-group markets, prior-year claims experience influences future premiums; in ACA-compliant small-group markets, health status cannot be used as a rating factor, but age, tobacco use, family size, and geography still apply

Pharmacy: The Fastest-Growing Cost Category

According to Mercer, pharmacy benefit costs rose 7.7% in 2024 following an 8.4% increase in 2023. Nationally, net U.S. medicine spending climbed from $548 billion in 2024 to $606 billion in 2025, a 10.6% jump in a single year, per IQVIA.

Specialty drug utilization is accelerating this trend. KFF found that 18% of large employers already cover GLP-1 agonists primarily for weight loss, with a third anticipating significant prescription drug spending impact. For a growing share of employers, pharmacy spending now rivals medical claims as a top budget line item.

Cost-Reduction Strategies for Group Health Insurance

The right strategies depend on where costs are actually originating. Sustainable reduction typically requires working across three dimensions: plan design decisions, how the plan is managed operationally, and the structural context in which coverage is purchased.

Strategies That Change Plan Design Decisions

These interventions reset the cost baseline rather than trimming it incrementally — which makes them the highest-leverage place to start.

Switch to an HDHP paired with an HSA

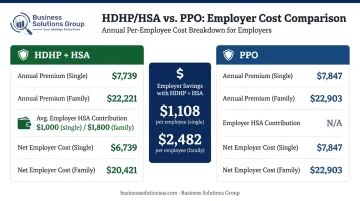

KFF data shows HDHP/SO plans average $8,275 for single coverage compared to $9,383 for PPO — a $1,108 difference per employee annually. For family coverage, that gap widens to $2,482.

The trade-off is real: HDHPs shift more out-of-pocket expense to employees through higher deductibles (minimum $1,650 individual / $3,300 family in 2025). Pairing the plan with employer-seeded HSA contributions — KFF reports employers contribute an average of $705 for single and $1,297 for family coverage — offsets that burden and keeps the overall benefit competitive.

This approach works best for healthier, younger workforces. Employees managing chronic conditions may find the financial exposure harder to absorb.

Restructure deductibles and copays based on utilization data

Many employers maintain low-deductible, low-copay plans because they always have — not because their workforce actually uses the plan heavily enough to justify the premium cost. Reviewing actual utilization before renewal can reveal significant room to adjust cost-sharing levers without meaningfully affecting most employees' out-of-pocket experience.

Shop carriers competitively at every renewal

Accepting a carrier's proposed renewal without alternative quotes means paying more than necessary. Bidding out coverage creates competitive pressure and often surfaces better-structured plans. Mid-year carrier changes are possible under certain conditions and worth exploring when a plan is materially underperforming.

Redesign pharmacy benefit tiers

Formulary structure, generic substitution incentives, and specialty drug management are all controllable levers. Generic and biosimilar medicines saved the U.S. healthcare system $467 billion in 2024, according to the Association for Accessible Medicines — most of that value comes from formulary design that actively steers utilization toward lower-cost alternatives. Working with a broker or PBM to audit and adjust formulary tiers regularly is one of the more direct ways to address the pharmacy cost trend.

Strategies That Change How the Plan Is Managed

Working within the existing plan structure, these approaches close the gap between what a plan costs on paper and what it actually delivers in practice.

Invest in employee education

Employees who understand their plan make cheaper decisions — not because they're cutting corners on care, but because they know when urgent care is appropriate versus an ER, how to request generic substitutions, and how to verify in-network status before booking appointments. Those behavioral differences compound across an entire workforce over a full plan year.

Make telehealth the default for non-emergency care

Telehealth visits are structurally less expensive than in-person care and eliminate the productivity loss of time away for appointments. Positioning telehealth as the first step for non-emergency issues — supported by zero or low copays — redirects a portion of claims away from higher-cost sites of care. Business Solutions Group's Employer Preventive Health and Tax Advantage Program includes telemedicine access with reduced or no copays as a core component, specifically to address this utilization dynamic.

Implement disease management and wellness programs — strategically

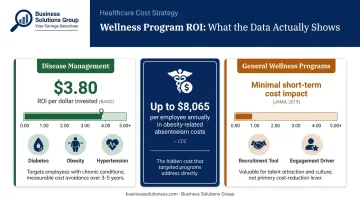

Broad wellness programs don't uniformly reduce costs. RAND found disease management generated $3.80 in savings per dollar invested, while lifestyle management alone produced much weaker results. A 2019 JAMA study found no significant short-term effect on healthcare spending from a general workplace wellness program after 18 months.

Programs targeting specific chronic conditions — diabetes, obesity, hypertension — show measurable ROI. General wellness programming is better framed as a recruitment and engagement tool than a cost-reduction strategy. CDC data puts obesity-related absenteeism costs at up to $8,065 per affected employee annually for a 100-person employer, which illustrates the scale of the underlying risk the right programs address.

Analyze claims data before every renewal

Employers who review their claims data before negotiating with carriers — understanding what's being claimed, at what frequency, and by whom — can target interventions more precisely, negotiate from a position of knowledge, and catch cost trends before they become structural problems.

Business Solutions Group's process includes ongoing program management review and reporting at weekly, monthly, or quarterly intervals, giving clients the data visibility needed to make these adjustments proactively rather than reactively.

Strategies That Change the Purchasing Context

Plan design and management matter, but the purchasing context often determines how much leverage an employer has before negotiations even begin.

Access large-group pricing through PEOs or associations

Small and mid-sized employers typically pay higher per-capita premiums because they lack the bargaining leverage of larger groups. Joining a professional employer organization (PEO) or industry association health plan can provide access to pricing and carrier relationships normally reserved for much larger buyers. NAPEO, which represents PEOs, reports health-benefit savings of $654 per FTE annually through PEO arrangements — though that figure comes from a trade association source and should be evaluated with that in mind.

Add voluntary and ancillary benefits to shift cost-sharing

Supplemental benefits — dental, vision, short-term disability, life insurance — funded primarily by employees add perceived value to the total package without increasing the employer's core healthcare spend. They can also reduce pressure on the primary medical plan by channeling certain claims through separate coverage.

Use spend benchmarking to negotiate from data, not intuition

Most employers don't know whether they're overpaying relative to comparable groups in their region and industry. A structured benchmarking analysis of healthcare spend against market norms exposes pricing inefficiencies and creates a factual basis for carrier negotiation. This is the same spend intelligence discipline Business Solutions Group applies across cost categories — from parcel and freight to healthcare — and it's effective in benefits procurement because carriers rarely volunteer that a group is above market.

Business Solutions Group's broader advisory practice applies detailed spend analysis to identify where clients are paying retail when wholesale pricing is available — their healthcare cost reduction program targets savings of $100–$300+ per employee per month for qualifying businesses with 25 or more employees.

Conclusion

Lowering group health insurance costs isn't a single conversation at renewal. It requires identifying where costs originate — plan design choices, how the plan is used day-to-day, or the structural disadvantages of how coverage is purchased — and addressing each layer deliberately.

Employers who treat benefits as an annual checkbox will consistently overpay. Those who bring the same analytical discipline to healthcare spend that they apply to other major cost categories find real, lasting savings — and keep the coverage their employees actually need.

Frequently Asked Questions

How can I reduce the amount I pay for health insurance premiums?

Employers can reduce premiums by switching to high-deductible plan designs, shopping carriers competitively at renewal, adjusting deductibles and copays based on actual workforce utilization, and benchmarking current spend against market rates. Stacking multiple strategies together consistently delivers larger, more durable savings.

Is $800 a month a lot for health insurance?

KFF 2024 data shows average monthly premiums of $746 for single coverage and $2,131 for family coverage. At $800/month, you're slightly above the single-coverage average — but whether that's high depends on whether it covers an individual or family, what the employer versus employee contribution split looks like, and the plan type and geographic market.

What is the most cost-effective group health insurance plan for small businesses?

HDHPs paired with HSAs are generally the most premium-efficient option — KFF data shows HDHP premiums average $1,108 less per year for single coverage compared to PPOs. Whether they're the right fit depends on workforce age, health utilization patterns, and whether employees can absorb higher deductibles.

Does offering a high-deductible health plan always save money?

HDHPs lower employer premiums but shift more out-of-pocket exposure to employees. They work best for healthier, younger workforces and should always be paired with HSA contributions and employee education. For workforces with higher chronic condition burdens, employee financial hardship risk can outweigh the premium savings.

How does group size affect health insurance premiums?

Larger groups benefit from risk pooling and greater carrier negotiating leverage, which produces lower per-capita premiums. Smaller employers can access comparable pricing through PEOs, industry association health plans, or group purchasing arrangements designed to aggregate buying power.

Can employers negotiate group health insurance rates with carriers?

Yes — particularly when armed with claims data, competitive quotes from alternative carriers, and a clear picture of the group's risk profile. Bundling medical, dental, and vision coverage and demonstrating stable retention also strengthens your negotiating position.