The frustrating part: telecom infrastructure is not inherently expensive. Costs escalate primarily through poor procurement discipline, absent spend visibility, and infrastructure that outlives its business case. Each of those drivers has a specific fix.

This article breaks down where telecom costs originate, which cost drivers have the most impact, and which strategies — across procurement, management, and infrastructure architecture — deliver the clearest results heading into 2026.

Key Takeaways

- Telecom costs compound through auto-renewals, idle assets, and deferred decisions, accumulating across billing cycles rather than hitting as a single budget event

- The biggest structural drivers are vendor fragmentation, legacy hardware dependency, and capacity over-provisioning

- The highest-leverage cost strategies are pre-contract — benchmarking, negotiation prep, and scope alignment before ink dries

- Cloud migration, centralized expense management, and contract benchmarking are the three most evidence-supported levers

- Cost reduction requires ongoing governance — quarterly usage reviews and annual contract audits at minimum

How Telecom Infrastructure Costs Typically Build Up

Most telecom overspend doesn't arrive as a line item anyone approved. It accumulates.

A contract auto-renews at last year's rates. A phone line stays active after a department restructures. A bandwidth commitment sized for projected peak load never gets right-sized once actual usage patterns stabilize. Individually, none of these is a serious mistake. Together, they compound into a cost structure that's genuinely difficult to untangle.

One unreviewed vendor contract quietly introduces duplicated services. Those duplicates pull in support overhead, which eventually requires additional tooling to manage. By the time a spending audit surfaces the problem, the organization is carrying compounded costs from a single lapse in procurement oversight.

What makes this particularly costly is that most of these charges remain invisible until something forces a review:

- A budget pressure event triggers a line-by-line spend analysis

- A system failure exposes how many redundant services were carrying identical functions

- A contract renewal forces a vendor relationship assessment that hadn't happened in years

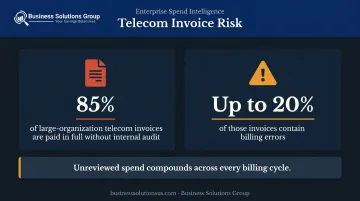

Crown Commercial Service's telecom audit research found that 85% of large-organization telecom invoices are paid in full without internal audit, with Gartner estimates suggesting up to **20% of those invoices contain billing errors**. That data is older, but the mechanism it describes — unreviewed spend accumulating across billing cycles — is structurally unchanged.

Organizations that audit reactively — only when budgets break — will consistently overpay relative to their actual infrastructure utilization.

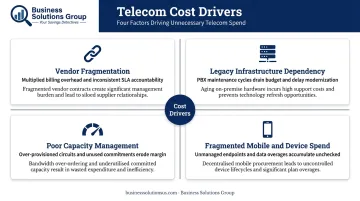

Key Cost Drivers for Telecom Infrastructure

No single driver dominates across all organizations. The weight of each depends on company size, geographic footprint, and how much infrastructure decision-making is centralized. That said, four drivers appear consistently.

Vendor Fragmentation

Managing multiple regional carriers under separate contracts creates compounding overhead at every level:

- Each relationship carries its own billing cycle, SLA terms, and reconciliation process

- Dispute resolution and compliance tracking multiply with every vendor added

- No single team owns the full picture of what's being paid or whether services are still needed

- Volume leverage — the most effective tool in carrier negotiations — disappears entirely

Legacy Infrastructure Dependency

The on-premises PBX market still represented $1.9 billion in 2024, though it declined 6.6% year-over-year, according to Metrigy. Companies with 10,000 or more employees accounted for 39.9% of remaining on-premises PBX revenue — and notably, 51.6% of on-premises users had no plans to replace their primary vendor.

Legacy voice systems carry costs beyond their visible maintenance contracts: dedicated IT labor, hardware refresh cycles every five to seven years, and structural limits on scalability. These are costs that grow over time without improving what the system can do.

Poor Capacity Management

Over-provisioning is a procurement assumption problem, not a usage problem. Organizations size bandwidth, line counts, and SIP trunks to projected peak demand — then never revisit those commitments as actual usage data accumulates.

The result is organizations paying for capacity they don't use throughout multi-year contract terms. One NHS Trust example from Crown's research found 27% of its mobile estate had zero usage — a concrete illustration of what happens when procurement projections don't get reconciled against reality.

Fragmented Mobile and Device Spend

Mobile endpoint costs — data overages, unmanaged device lifecycles, unsanctioned carrier upgrades — frequently sit outside central IT visibility. They grow as a parallel cost problem alongside core infrastructure spend, typically undetected until a consolidated audit brings all telecom categories into a single view — at which point the scale of unmanaged spend becomes clear.

Cost-Reduction Strategies for Telecom Infrastructure

Effective cost reduction depends on where in the lifecycle costs originate. Strategies must be matched to their source — applying a procurement fix to a management problem, or vice versa, wastes effort and rarely produces durable results.

Strategies That Change Decisions Before Costs Are Set

These approaches carry the highest leverage because they shape the cost baseline before infrastructure is deployed or contracts are signed.

Benchmark before every renewal. Without a credible market benchmark, organizations negotiate blind — and carriers have no incentive to volunteer favorable pricing. Pre-renewal benchmarking establishes what comparable organizations actually pay for equivalent services. Business Solutions Group's spend intelligence capabilities and benchmark analysis are designed exactly for this: establishing a market baseline before clients enter any carrier negotiation.

Consolidate vendors before renegotiating. Identify all active telecom service providers across locations and business units, then assess where consolidation to fewer primary carriers is feasible. Consolidation delivers two advantages simultaneously:

- Stronger volume leverage with remaining carriers

- Lower administrative overhead from managing fewer relationships — without reducing service coverage

Right-size capacity at procurement. Review bandwidth commitments, line counts, and data allocations against 12–18 months of actual usage data before renewing. Correcting over-provisioning at contract time costs nothing. Carrying unused capacity through a three-year term costs significantly more.

Build flexibility into contract terms. Negotiate for shorter initial terms with renewal options, usage-based pricing tiers where available, and downsize provisions that don't trigger penalties. Rigid long-term contracts lock in costs that should decrease as technology and competition evolve.

Strategies That Improve Management of Active Infrastructure

These strategies address costs that emerge after procurement and compound without active oversight.

Centralize telecom expense management. Consolidating billing, usage data, and contract terms into a single management system enables anomaly detection, billing dispute resolution, and consistent policy enforcement.

Decentralized management — where each department or location handles its own vendor relationships — structurally prevents this visibility. Business Solutions Group's spend intelligence and advisory services help organizations consolidate that data, eliminating the need to reconcile costs across disconnected portals or spreadsheets.

Audit usage and deactivate idle assets on a schedule. Idle phone lines, inactive SIP trunks, and unassigned device licenses accumulate quickly without formal review processes. Quarterly reviews to identify and retire assets that no longer serve an active business function are a minimum standard. The Crown research example — one organization incurring £1 million in charges for ceased services — illustrates how long idle assets can generate charges when no one is looking.

Automate invoice validation. Manual invoice review is prone to error and delay. Billing discrepancies and overcharges go undetected across billing cycles when reconciliation depends entirely on human review. Automated monitoring flags anomalies in real time and generates dispute evidence before billing cycles close.

Business Solutions Group's spend intelligence software addresses this directly — continuously identifying credits and recovering overcharges, with clients receiving 100% of those returns.

Integrate mobile management into enterprise telecom governance. Mobile spend belongs in the same governance framework as wireline and cloud spend. Without integration, it becomes a parallel cost problem reviewed separately — and less rigorously. That gap compounds quickly across large device fleets.

Strategies That Change the Infrastructure Context

These approaches address the surrounding architecture and environment that drives telecom spend, not just the services themselves.

Migrate from legacy on-premises systems to cloud-based infrastructure. On-premises PBX carries hidden costs well beyond maintenance contracts: the IT labor to manage it, hardware refresh capital every five to seven years, and the ceiling it places on scalability. Cloud-native alternatives convert those fixed infrastructure costs into variable operating expenses.

The financial case for migration comes primarily from vendor-commissioned studies — useful as directional evidence, not universal benchmarks:

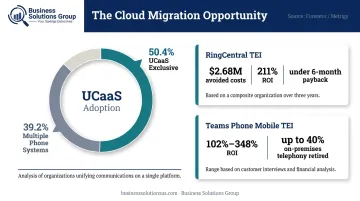

- Forrester Consulting's 2023 TEI for RingCentral modeled $2.68 million in avoided legacy system costs over three years, 211% ROI, and payback under six months

- A 2024 Forrester TEI for Microsoft Teams Phone Mobile modeled 102%–348% ROI and retirement of up to 40% of on-premises telephony services

Metrigy's current adoption data shows 50.4% of businesses now use UCaaS exclusively, while 39.2% still operate multiple phone systems — meaning consolidation and migration opportunities remain substantial across the enterprise market.

Implement intelligent call routing. In multi-location or geographically distributed environments, routing based on origin, destination, and carrier cost — rather than default path selection — avoids unnecessary PSTN, toll, and international charges. Exact per-minute savings vary by environment and carrier mix, but the approach is well-proven in distributed deployments.

Address energy costs as an infrastructure line item. Power consumption from networking equipment and remote telecom sites is a growing share of total infrastructure operating cost. The Uptime Institute's 2024 global data center survey reported an industry average data center PUE of 1.56, with 25% of data centers running below 40% UPS capacity utilization. For organizations with significant on-premises or distributed telecom infrastructure, equipment consolidation and PUE improvements are direct OPEX levers — not just sustainability considerations. The IEA projects data center energy demand could exceed 1,000 TWh by 2026, roughly double 2022 levels, which will push energy cost pressure further into infrastructure budgets.

Conclusion

Reducing telecom infrastructure costs for 2026 requires correctly identifying where cost originates — across procurement decisions, active management practices, and the infrastructure architecture itself. Blanket budget cuts misallocate effort and often degrade service quality without addressing what's actually driving the spend.

The organizations that consistently outperform on telecom cost control treat it as a continuous practice:

- Benchmark contracts before renewal windows open

- Conduct quarterly usage reviews

- Govern mobile and enterprise telecom spend from a unified platform

Finance, IT, and operations need to be aligned on the same data, not working from separate views of the same vendor relationships.

For organizations ready to move from reactive spending to structured optimization, a conversation with Business Solutions Group is a practical starting point. Their benchmark analysis and cost advisory services establish spend visibility before any contract decision is made — which is where cost control carries the most weight.

Frequently Asked Questions

What is the most effective first step in reducing telecom infrastructure costs?

A comprehensive usage and spend audit. Without knowing which services are active, which are idle, and what each actually costs against current market rates, no optimization strategy can be accurately targeted. Business Solutions Group offers a free benchmark analysis as an entry point for organizations that lack this baseline.

How much can businesses typically save by consolidating telecom vendors?

Consolidation drives savings two ways: better pricing through volume leverage with fewer carriers, and lower administrative overhead. Business Solutions Group's telecom expense management engagements typically deliver 20–50% savings, depending on the starting complexity of the vendor environment.

What is the difference between CAPEX and OPEX reduction in telecom infrastructure?

CAPEX reduction targets one-time infrastructure investments — hardware, physical build-out, on-premises assets. OPEX reduction targets recurring costs: contracts, maintenance, energy, and labor. Most organizations have more near-term leverage in OPEX, while CAPEX reduction through cloud migration or infrastructure sharing requires longer planning horizons.

Can businesses reduce telecom costs without switching carriers?

Yes. Contract renegotiation, right-sizing, usage audits, and automated invoice validation can produce significant savings with existing providers. Benchmark data is often the most persuasive tool — showing a carrier where its pricing sits relative to market rates creates a basis for renegotiation that carriers otherwise have no incentive to offer.

How does cloud migration affect telecom infrastructure costs?

Cloud-based telecom converts fixed capital and maintenance costs into variable operating expenses, eliminating hardware refresh cycles and enabling capacity to scale without proportional cost increases. Vendor-commissioned Forrester TEI studies put ROI at 102% to over 200% over three years, depending on the legacy system being replaced.

How often should organizations audit their telecom infrastructure spend?

At minimum, quarterly usage reviews for active assets and an annual contract review tied to renewal windows. Organizations without automated monitoring tools often discover months of avoidable overcharges only after a formal audit is triggered, well after the costs have accumulated.